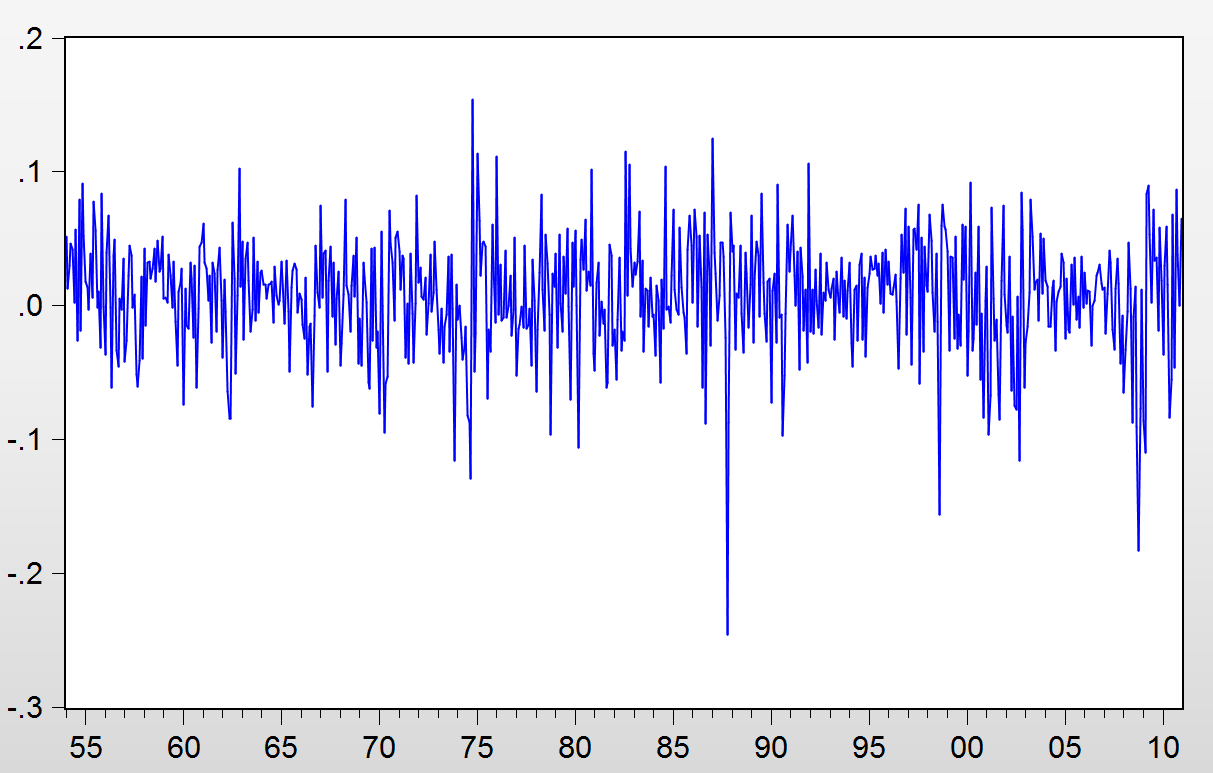

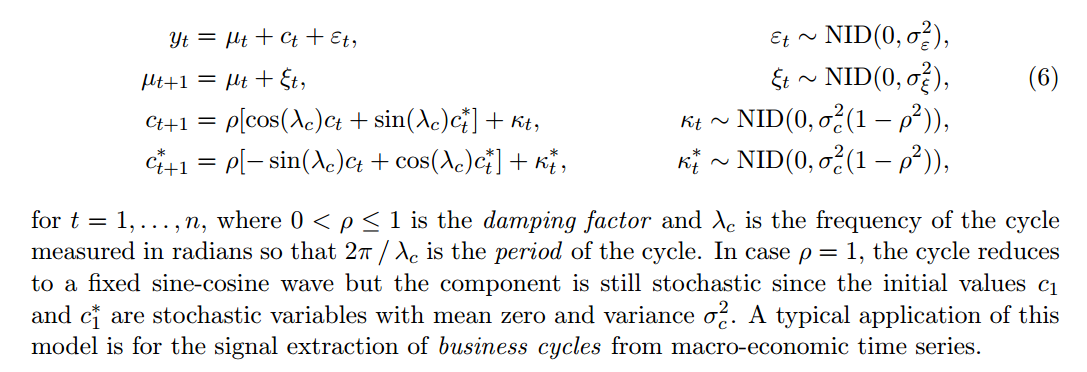

I am trying to specify a state space model for the dependent variable from this graph. As you can see, there clearly seems to be cyclical behaviour. Therefore, I tried to specify the following state space model:

However, I am not sure what I should use for lambda. Does anyone know what this value should approximately be for the data in the plot (the data is monthly)?

For those who are interested, I am using the following code in EViews

@SIGNAL SP500EP = mu + c1 + beta1*x1(-1)^2+ [var = exp(C(1))]

@state mu = mu(-1) + [var = exp(C(2))]

@STATE c1 = c(3)*(@cos(0.00001)*c1(-1) + @sin(0.00001)*c2(-1)) + [var = exp( c(4)*(1 - c(3)^2) ) ]

@STATE c2 = c(3)*(-@sin(0.00001)*c1(-1)+ @sin(0.00001)*c2(-1)) + [var = exp( c(4)*(1 - c(3)^2) ) ]

@state beta1 = beta1(-1)

@param c(1) 3 c(2) 3 c(3) 3 c(4) 3 c(5) 3 c(6) 3 c(7) 3

As you can see I am currently using the value 0.00001 for lambda as this seems to give the best results but I doubt if its logical. If anyone has any other suggestions for state space models that can capture the cycle from the plot, that would also be helpful!

Thank you in advance!

Edit:

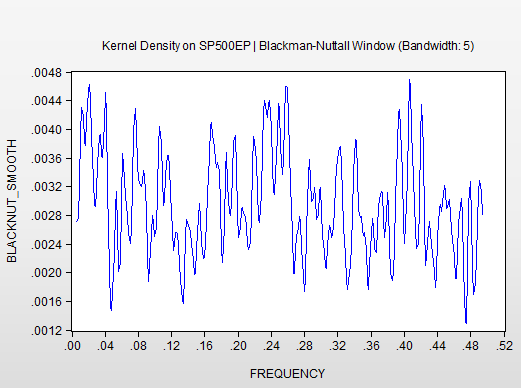

Following up on F. Tusell's suggestion, here the periodogram of the data, can anyone tell me what exactly this tells me about what I should pick for lambda?