According to a least squares fit I have performed to my data, my slope is $-0.1038±0.033$, and my offset $0.1065±0.032$. My first idea was to visualise this by drawing three lines: $0.1065-0.1038x$, $(0.1065+0.032) - (0.1038-0.33)x$, and $(0.1065-0.032) + (0.1038+0.33)x$. Those correspond to the 95% confidence interval. However, the joint probability that both slope and offset are at the edge of the 95% intervals is certainly not 5%. If the two were independent it would be closer to 0.25%, whereas in reality the joint probability is probably somewhere in-between.

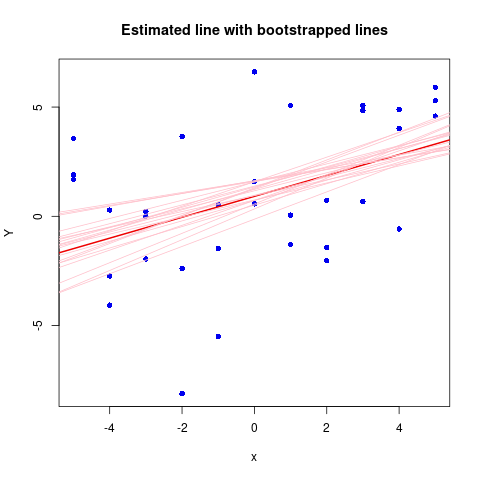

I could calculate the confidence interval at $\sqrt{0.05}$ for offset and slope and then visualise the extrema as described above, to get an effective 5% probability range. But I'm almost certainly reinventing the wheel here. What is a suitable way of visualising the uncertainty in a regression line — slope and offset?

For reference, Pythons statsmodels.api.OLS summaries my regression fit as below. In my real world example, I use a weighted least squares, because I have errors on my y-values (and I am considering orthogonal distance regression as I have errors on my x-values too, but I am neglecting those for now).

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.026

Model: OLS Adj. R-squared: 0.023

Method: Least Squares F-statistic: 9.673

Date: Mon, 06 Apr 2015 Prob (F-statistic): 0.00202

Time: 18:14:55 Log-Likelihood: 1223.1

No. Observations: 370 AIC: -2442.

Df Residuals: 368 BIC: -2434.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [95.0% Conf. Int.]

------------------------------------------------------------------------------

const 0.1065 0.032 3.343 0.001 0.044 0.169

x1 -0.1038 0.033 -3.110 0.002 -0.169 -0.038

==============================================================================

Omnibus: 23.030 Durbin-Watson: 1.484

Prob(Omnibus): 0.000 Jarque-Bera (JB): 45.433

Skew: -0.350 Prob(JB): 1.36e-10

Kurtosis: 4.567 Cond. No. 138.

==============================================================================