I've got 2 questions about this. I'm fitting a VAR in levels in order to select lag length for Johansen cointegration tests. All my data are in natural logarithms.

1) All my variables are I(1) except an exogenous variable that is I(0), is a stock that is growing but at a diminishing rate. Do I include this variable as an exogenous variable in the VAR (and can I include it in Stata in the VECM for cointegration?)

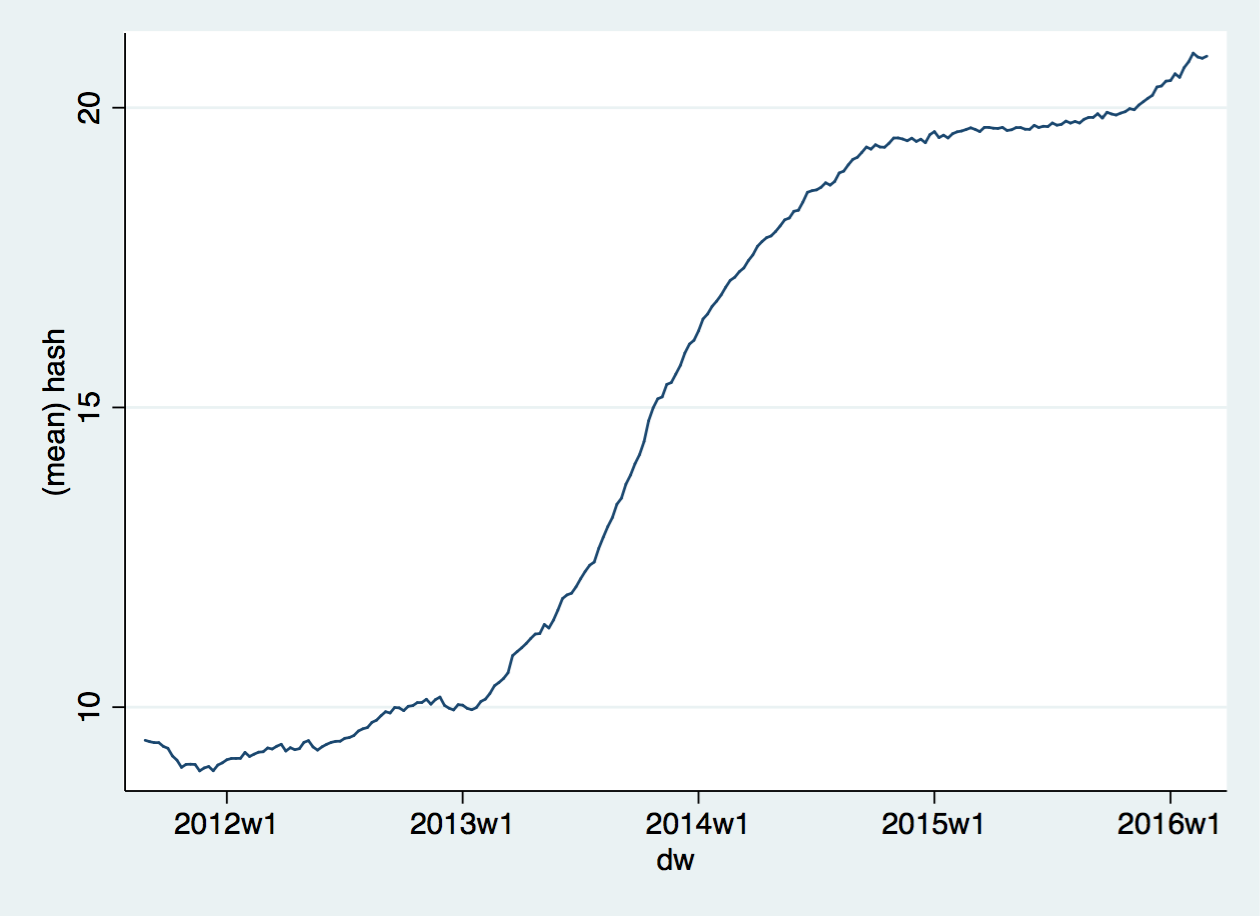

2) How do I deal with the changing trend in the graph below? (The mean label simply refers to the fact that the data have been converted from daily to weekly so ignore that). The techniques I know for dealing with structural breaks don't really work for this.

Any help much appreciated!