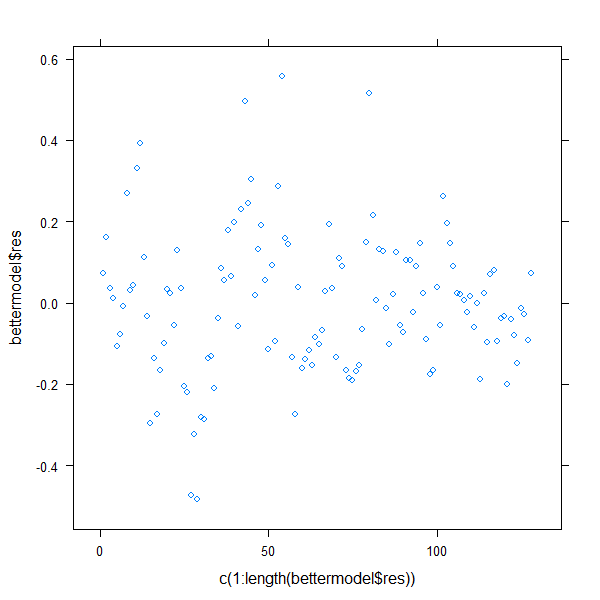

I have a OLS model that I try to prove it has cointegration between two regressors and the dependent variable. The model fits well, with a very high $R^2$. The residuals don't seem to be autocorrelated.

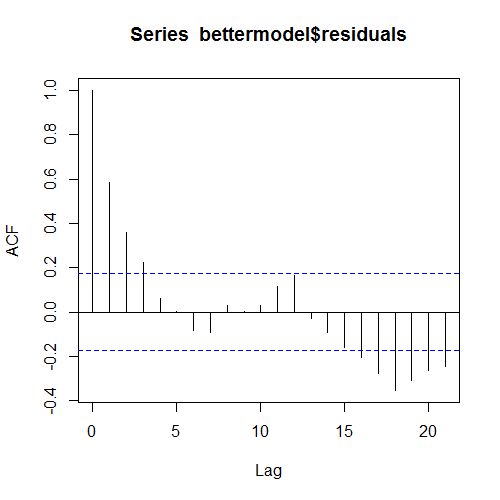

FYI, I only have 135 data points for the dependent variable. The model residuals pass KPSS, ADF and PP test to be stationary, but Durbin–Watson test fails:

> tseries::adf.test(bettermodel$res)

Augmented Dickey-Fuller Test

data: bettermodel$res

Dickey-Fuller = -4.2461, Lag order = 5, p-value = 0.01

alternative hypothesis: stationary

Warning message:

In tseries::adf.test(bettermodel$res) :

p-value smaller than printed p-value

> tseries::kpss.test(bettermodel$res)

KPSS Test for Level Stationarity

data: bettermodel$res

KPSS Level = 0.0843, Truncation lag parameter = 2, p-value = 0.1

Warning message:

In tseries::kpss.test(bettermodel$res) :

p-value greater than printed p-value

> tseries::pp.test(bettermodel$res)

Phillips-Perron Unit Root Test

data: bettermodel$res

Dickey-Fuller Z(alpha) = -53.7486, Truncation lag parameter = 4, p-value= 0.01

alternative hypothesis: stationary

Warning message:

In tseries::pp.test(bettermodel$res) : p-value smaller than printed p-value

> lmtest::dwtest(bettermodel)

Durbin-Watson test

data: bettermodel

DW = 0.8288, p-value = 0.000000000003394

alternative hypothesis: true autocorrelation is greater than 0

I feel confused about this and I am not sure whether my model selection satisfies the condition of cointegration. Any thoughts?