The QuantReg family of the mboost package has two parameters: tau (the target quantile) and qoffset (quantile of response distribution to be used as offset). The default for both parameters is 0.5. Should I change the qoffset parameter if I estimate another quantile? For example, if I want to estimate the 0.95 quantile, should I set qoffset = 0.95?

$\begingroup$

$\endgroup$

$\endgroup$

asked May 31, 2016 at 6:53

Add a comment

|

1 Answer

$\begingroup$

$\endgroup$

(Of note, we had this discussion already offline but to close this issue and let others know, I will restate the results here)

The qoffset argument can be used to determine a good starting value for (the intercept of) the boosting algorithm. qoffset computes the qoffset-quantile of the response

quantile(y[rep(1:length(y), w)], qoffset)

which is then used as initial value for the intercept.

As stated in the related JASA publication [1]:

(...) starting values, (...) have to be chosen. While it is natural to initialize all effects at zero, it turns out that faster convergence and more reliable results are obtained by defining a fixed offset as a starting value for the intercept. An obvious choice may be the tau-th sample quantile of the response variable but our empirical experience suggests that the median is more suitable in general, as will be illustrated in an example in Section 3.

On p17 of the e-supplement of the article it is stated:

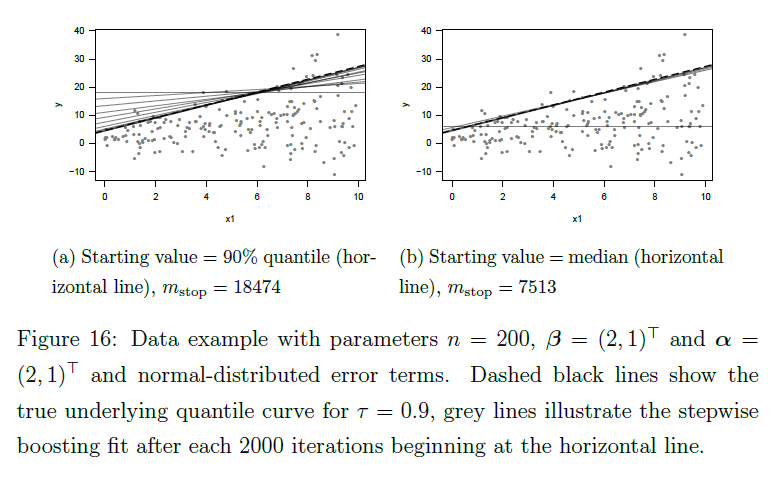

(...) we decided to take the median as starting value for the intercept instead of the tau-th sample quantile of the response variable. This decision was based on the following empirical results. For quantiles smaller than tau = 0.5, we explored hardly any differences between resulting mstop criteria and estimators for beta_tau depending on the starting values. However, for quantiles larger than tau = 0.5 the mstop criterion was dramatically increased when taking the tau-th sample quantile as starting value. As an example, Figure 16 illustrates the stepwise approach of the boosting estimation to the true underlying 90% quantile curves depending on the starting value. Note that it takes considerably more iterations until the estimation approaches the true quantile curve when beginning at the 90% sample quantile, shown in Figure 16(a). On the contrary, Figure 16(b) displays that the estimation converges much faster when beginning at the median.

So one can deduce that you can leave this value as is. I've added a note in the manual of the mboost 2.7-0 [2].

[1] Nora Fenske, Thomas Kneib, and Torsten Hothorn. "Identifying Risk Factors for Severe Childhood Malnutrition by Boosting Additive Quantile Regression". Journal of the American Statistical Association Vol. 106 , Iss. 494,2011. DOI http://dx.doi.org/10.1198/jasa.2011.ap09272