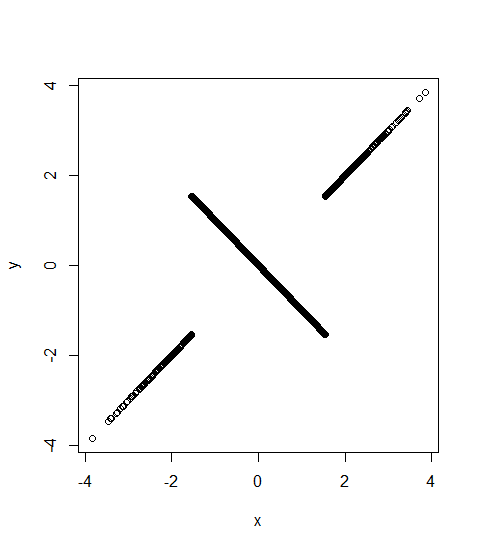

I am looking for an example of 2 random variables $X$, $Y$ such that

$$\newcommand{\cor}{{\rm cor}}|\cor(X,Y)| \approx 0 $$

but when consider the tail part of the distributions, they are highly correlated. (I try to avoid 'correlated' / 'correlation' for the tail because it might not be linear).

Probably use this:

$$|\cor(X', Y')| \gg 0$$

where $X'$ is conditional on $X > 90\%$ of $X$'s population, and $Y'$ is defined in the same sense.