Can the unit root test of Dickey-Fuller be used even when the residuals are not normally distributed?

$\begingroup$

$\endgroup$

1

-

$\begingroup$ To make it a more interesting thinking process I ask a couple of simpler question: can we use OLS to estimate a simple bivariate regression when the variables are not normal? What does Gauss-Markov Theorem say about OLS and what assumptions does one make? $\endgroup$– Math-funCommented Jan 9, 2017 at 16:06

Add a comment

|

2 Answers

$\begingroup$

$\endgroup$

$\endgroup$

5

Yes, that is not a necessary condition. Recall that all we know about the null distribution of the Dickey-Fuller test is its asymptotic representation (although the literature of course considers many refinements).

As is often the case, we do not need distributional assumptions on the error terms when considering asymptotic distributions thanks to (in this case: functional) central limit theory arguments.

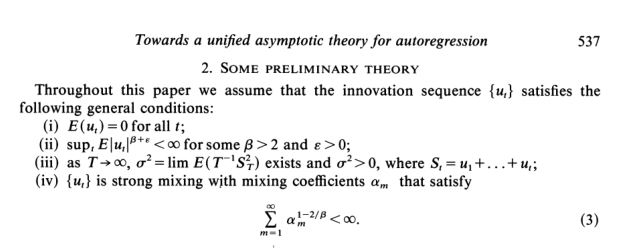

Here is a screenshot from Phillips (Biometrika 1987) stating assumptions on the errors - as you see, these are way broader than requiring normality.

That said, the asymptotic distribution does not have a closed-form solution, so that you need to simulate from the distribution to get critical values (existing infinite series representations are not practical either to generate critical vales). To perform that simulation, you must draw erros from some distribution, and the conventional choice is to simulate normal errors.

But, as Phillips shows, if you were to draw the errors from some other distribution satisfying the above requirements, you would asymptotically get the same distribution. You could replace the line with rnorm(T) with some such distribution in my answer here to verify.

That said, the finite-sample distribution will of course be affected by the error distribution, so that the error distribution will play a role in shorter time series. (Indeed, I did replace rnorm(T) with rt(T, df=8), and differences are still relevant for $T$ as large as 20.000.)

answered Dec 9, 2016 at 8:41

-

$\begingroup$ I am looking for practical guidelines regarding the use of Dickey-Fuller test, and @mlofton suggests (here and above) that (roughly speaking) normality cannot be assumed away. That seems to clash with your answer. How do I reconcile the two? Is one of these incorrect? $\endgroup$ Commented Aug 12, 2020 at 11:20

-

$\begingroup$ I do not think there is a clash. My answer cites the asymptotic distribution, which does not assume normal errors, as Phillips' theorems unequivocally show. That said, the asymptotic distribution does not have a closed-form solution, so that you need to simulate from the distribution to get critical values (existing infinite series representations are not practical either to generate critical vales). To perform that simulation, you must draw erros from some distribution, and the conventional choice is to simulate normal errors. But, as Phillips shows, if you were to draw the errors from... $\endgroup$ Commented Aug 12, 2020 at 14:30

-

$\begingroup$ ...some other distribution satisfying the above requirements, you would asymptotically get the same distribution. You could replace the line with

rnorm(T)with some such distribution in my answer here stats.stackexchange.com/questions/213551/… to verify. That said, the finite-sample distribution will of course be affected by the error distribution, so that the error distribution will play a role in shorter time series. $\endgroup$ Commented Aug 12, 2020 at 14:32 -

$\begingroup$ Thank you for a very clear explanation! Including it as an update to your answer might be a good idea. $\endgroup$ Commented Aug 12, 2020 at 14:53

-

$\begingroup$ Thanks Christoph: I never disagreed with your answer but thanks for clarification. Generally speaking, as you know, no one would ever use Phillips result because simulating analytically from the derived distribution is not terribly practical. People generally use the DF tables and those have nothing to do with asymptotic representation. They use the normality of the error term and allow the practitioner to obtain DF statistics for sample sizes as low as 20. Thanks though for clarification. $\endgroup$– mloftonCommented Aug 13, 2020 at 14:26

$\begingroup$

$\endgroup$

29

Yes, the innovations need not be normal, not at all.

The underlying mathematical fact that gives rise to the asymptotic null distribution of the DF statistic is Functional Central Limit Theorem, or Invariance Principle.

The FCLT, if you'd like, is an infinite dimensional generalization of the CLT. The CLT holds for dependent, non-normal sequences, and similar statement can be made about the FCLT.

(Conversely, FCLT implies CLT, as the finite dimensional distribution of the Brownian motion is normal. So any general condition that gives you a FCLT immediately implies a CLT.)

Functional Central Limit Theorem

Given a sequence of random variables $u_i$, $i = 1, 2, \cdots$. Consider the sequence of random functions $\phi_n$, $n = 1, 2, \cdots$, defined by $$ \phi_n(t) = \frac{1}{\sqrt{n}}\sum_{i = 1}^{[nt]} u_i, \; t \in [0,1]. $$ Each $\phi_n$ is a stochastic process on $[0,1]$ with sample paths in the Skorohod space $D[0,1]$.

The generic form of FCLT provides sufficient conditions under which $\{ \phi_n \}$ converges weakly on $D[0,1]$ to (a scalar multiple of) the standard Brownian motion $B$.

Sufficient conditions, which are more general than those from Phillips and Perron (1987) quoted above, were known prior, if not in the time series literature. See, for example, McLiesh (1975):

The strong mixing condition (iv) of Phillips and Perron implies McLiesh's mixingale condition under some conditions.

Condition (ii) of Phillips and Perron requiring uniform bound on $2 + \epsilon$ moments of $\{ u_i\}$ is relaxed in McLeish to the uniform integrability of $\{ u_i^2 \}$.

Condition (iii) of Phillips and Perron is actually not quite correct/sufficient as intended.

For a further milestone in the time series literature in this direction, see Elliott, Rothenberg, and Stock (1996), where they apply a Neyman-Pearson-like approach to benchmark the asymptotic power envelope of unit root tests. The normality assumption is long gone by then.

DF Statistic

It follows immediately from the FCLT and the Continuous Mapping Theorem that the DF $\tau$-statistic $\tau$ has the asymptotic distribution $$ \tau \stackrel{d}{\rightarrow} \frac{\frac12 (B(1)^2 - 1)}{ \sqrt{ \int_0^1 B(t)^2 dt} }. $$ The 5th-percentile of this distribution is the critical value for DF test with nominal size of 5%.

Simulating $\tau$ with an i.i.d. normal error term and another error term that follows, say, a time series specification would lead to the same distribution as sample size gets large.

Comment

I am going to disagree with @mlofton's comment that

Generally speaking, no one would ever use Phillips result because simulating analytically from the derived distribution is not terribly practical. People generally use the DF tables and those have nothing to do with asymptotic representation. They use the normality of the error term and allow the practitioner to obtain DF statistics for sample sizes as low as 20...

It's a major contribution of Phillips to point out that an "assumption free" asymptotic distribution is possible. This is one of the reasons, along with contemporary developments in economic theory, that convinced empirical practitioners (in particular, macro-econometricians) that unit root tests belonged to their everyday toolbox. A statistic (more specifically, a null distribution) that requires normality of the data generating process is not useful at all---e.g. suppose the $t$-statistic is only valid if data is i.i.d. normal. That was the limitation of the early unit root literature.

-

$\begingroup$ Hi Michael: I've already had a long discussion with Richard on this. My point is that, to use Phillips' result to claim that the DF tables don't assume normality, is not the correct thing to do. I'm pretty certain that the DF tables do assume normality ( see the link in Greene that I point to) but, the best thing to do would be to do EXACTLY what DF do, except with non-normal errors, and see if the same critical values are obtained. Note that the limitation of the early unit-root literature was that , under the unit root null, the t-statistic is not t-distributed when the errors are normal. $\endgroup$– mloftonCommented Aug 23, 2020 at 13:40

-

$\begingroup$ @mlofton "...to use Phillips' result to claim that the DF tables don't assume normality, is not the correct thing to do"---well, that is simply not true or correct. $\endgroup$– MichaelCommented Aug 23, 2020 at 13:45

-

$\begingroup$ I think it is but we can agree to disagree. And I'm sorry, the precvious link , I pointed to was DW test rather than DF. When I have time, I'll try to ask someone ( who can point me to somewhere that says yes or no ). whether DF assumes normality of error term. I'm pretty certain it does but the only place where it says so is Greene. As I said, best way to know would be through simulation. $\endgroup$– mloftonCommented Aug 23, 2020 at 13:55

-

$\begingroup$ @mlofton The statements in Phillips-Perron clearly says normality is not required at all, that's a basic fact (those results are plainly true, if not exactly under the conditions they claim). "...DF tables do assume normality..."---yes, in Dickey and Fuller (JASA 1979 and Econometrica 1981). That's why unit root tests were not widely considered by empirical folks prior to Phillips---it's not reasonable to have to always assume i.i.d. N(0,sigma^2) errors for a time series. The assumptions and derivations in those papers are very primitive by today's standards. $\endgroup$– MichaelCommented Aug 23, 2020 at 14:15

-

1$\begingroup$ Michael: That was a beautiful analogy. I get it now. Thanks so much and apologies. Also, my apologies to Peter Phillips also since what he did was a bigger deal than I ever realized. For those reading this, Hamilton's chapter on this topic is also quite good, although he doesn't explain the relation between Dickey Fuller, 1979 and Phillips results like Michael did. $\endgroup$– mloftonCommented Aug 27, 2020 at 13:32