Hello everyone I am an MSc student in economics and one of my modules is Econometrics I which seems to be proof based or what I think could be considered proof-based. Before asking my question here I asked my professor but he's in vacation and don't know when he's going to answer

Now, some of you may laugh at me but I having a hard time understanding a particular answer.

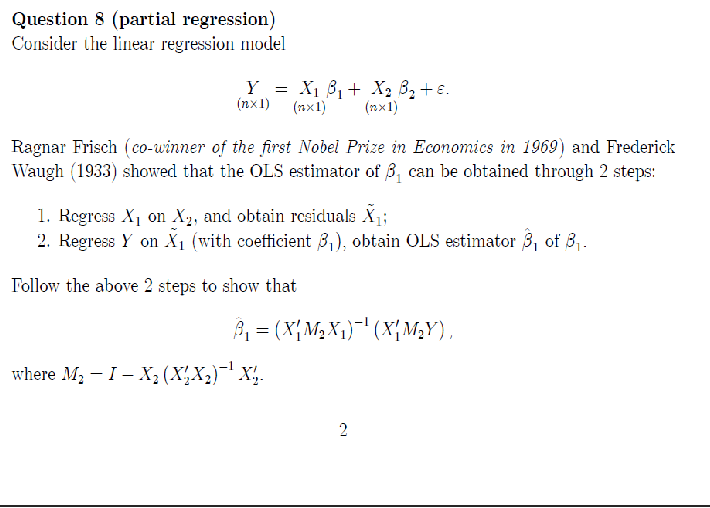

So I have this:

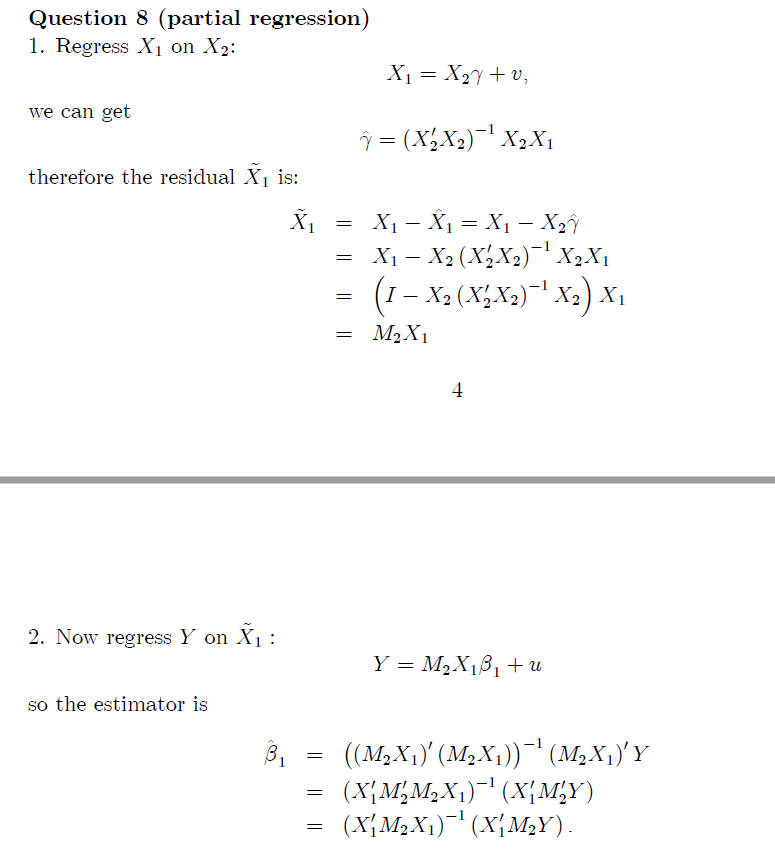

and this is the answer:

I don't understand what exactly are the steps he's taking, what does he mean to Regress X1 on X2? and how does he get that gamma hat? Sorry if these are silly questions but most of his answers are usually step-by-step and have no trouble understanding.

Also another questions is related to estimation of variance which is:

An unbiased estimator $\sigma^2 is: $s$^2$ = $\frac{SSR}{(n-k)}$ so the variance of $\beta$ hat = $s^2$(X'X$^-$$^1$)

Where does that s^2 come from? what is it's proof? and what exactly does it mean? What does s equal to? I apologize i'm asking this but I got an exam next year in early January and want to be prepared.

If someone can suggest a proof heavy book in econometrics that shows steps and whatnot it would be great since I mostly use the lecture slides which are really good.

I apologize for the long post.

And before anyone asks, I have a bad habit of not reading during the term/semester and end up asking questions barely at the end.