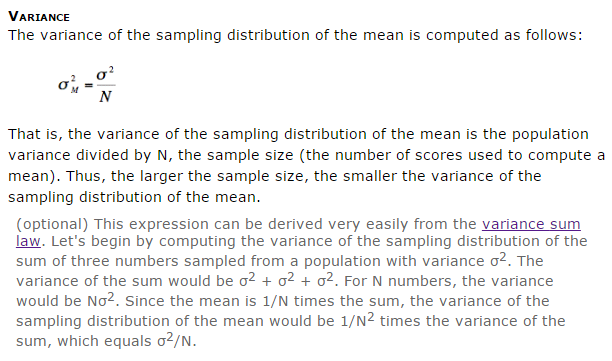

The sample $X_1,\dots,X_n$ of size $n$ is assumed to be iid (idependent and identically distributed) with mean $\mu$ and variance $\sigma^2$, i.e. $E(X_i) = \mu$ for every $i$ and $V(X_i) = \sigma^2$.

Consider the sample mean $$\bar X = \frac{1}{n}\sum_{i=1}^n X_i.$$

Expected value of that term is given by $$E(\bar X) = E\left(\frac{1}{n}\sum_{i=1}^nX_i\right) = \frac{1}{n}\sum_{i=1}^n E(X_i) = \frac{n}{n}\mu = \mu$$

where it was used that $E$ is linear (hence constant and sum can be taken out of the expectation) and that every $X_i$ has the same mean $\mu$.

The variance of the sample mean can be calculated similarily:

$$V(\bar X) = V\left(\frac{1}{n}\sum_{i=1}^nX_i\right) = \frac{1}{n^2}\sum_{i=1}^nV(X_i) = \frac{n}{n^2}\sigma^2 = \frac{\sigma^2}{n}.$$

The variance acts a little different than expecation though. The variance is not linear in its argument but homogen of degree 2, i.e. $V(aX) = a^2V(X)$. Furthermore, the variance of a sum of random variable is only the sum of variances if the random variables are pairwise uncorrelated (i.e. in particular if the random variables are independent).

I recommend going through the steps I provided and ask if there remains something unclear.

By the way, the sentence you don't understand the meaning of is not quite correct either as it asserts that the variance of a sum of random variables is the sum of random variables (times $1/n^2$). But as I stated this is only correct in the case of pairwise uncorrelated, or even stronger, idependent random variables.