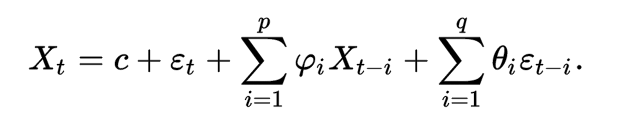

Here is the documentation for statsmodel's ARMA fit function. My issue is that it does not specify the form of the model it is fitting, i.e. is it fitting $a(L)y_t = b(L)\epsilon_t$ or is it fitting the regression form

It's a bit confusing because statsmodel's ARMA generation assumes the form $a(L)y_t = b(L)\epsilon_t$, but the "no constant" option makes it unclear.