I am building a model to explain performance in one time period to another. I have my variables and then I have an interaction effect for those variables in the second time period.

Using this data, I can then say what is the change in performance due to the change in these values ( this is split by the change in average in t0 and t1, and also the change in beta coefficients).

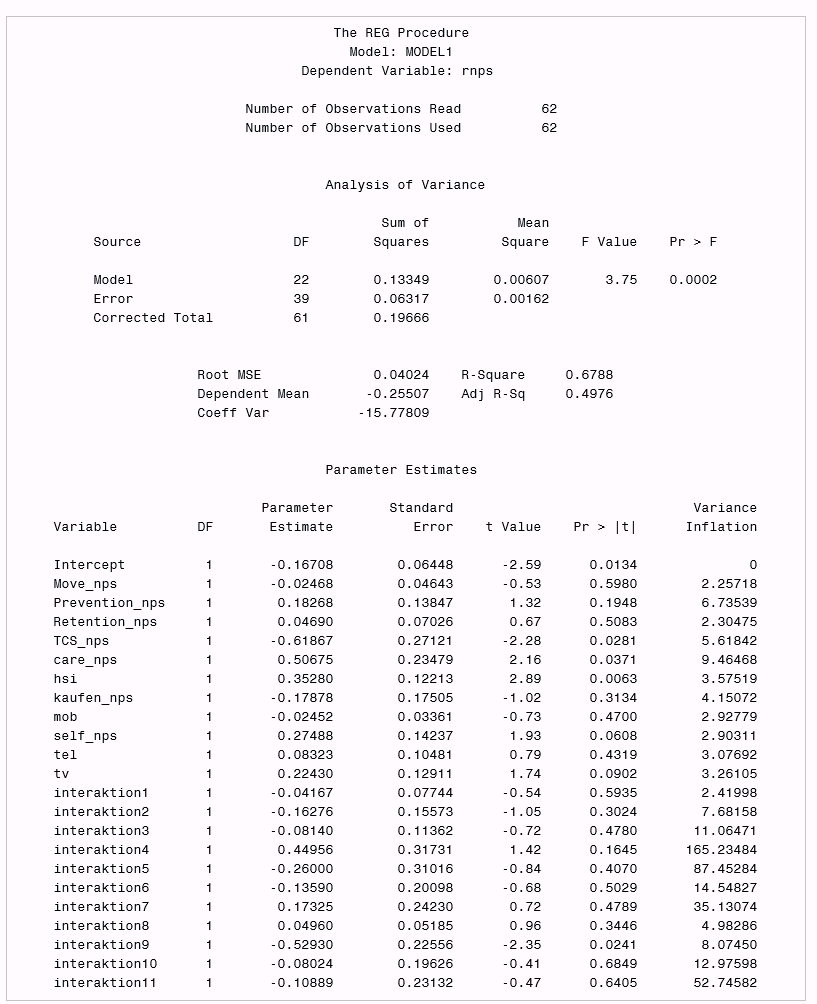

The challenge I have is that many values in t0 are significant (and have acceptable VIF). However when I look at the corresponding coefficients and their VIFs, they are incredible high - some over 100 and some over 500.

My simple question, can I use these values that are significant in t0 but have very high VIF in t1? What are the dangers of using them?

Part 2;

I have looked into using lasso to select the model. The challenge there is that it stops at 2 variables, when I can see that more are significant, and the best manual model I can build doesn't come through. I am also struggling to formulate this in SAS as I have when I have 3 variables ( var 1 var 2 var 3 and their corresponding interactions (int 1 int 2 int 3), lasso picks var1 and int 2 which doesn't work. I add this as an additional element, and can understand if you cannot answer it and I need to repost it in stack overflow. The first part is more important to me right now.

Part 2;

I have looked into using lasso to select the model. The challenge there is that it stops at 2 variables, when I can see that more are significant, and the best manual model I can build doesn't come through. I am also struggling to formulate this in SAS as I have when I have 3 variables ( var 1 var 2 var 3 and their corresponding interactions (int 1 int 2 int 3), lasso picks var1 and int 2 which doesn't work. I add this as an additional element, and can understand if you cannot answer it and I need to repost it in stack overflow. The first part is more important to me right now.