I am a freshman with Bayesian lasso. I searched online and found that the only package I can use is monomvn. There's only one example about diabetes data in its R document. However, the parameters set in that example is quietly simply. Just "blasso(x,y)". I tried to follow this but when it comes to my data, all coefficients were shrunk to zeros. Should I give initial values to beta? Appreciate it if anyone could provide examples describing how to set parameters for this function? Thanks a lot.

1

-

$\begingroup$ Questions about how to use software are generally off topic here, & tutorials are explicitly outside our mandate. $\endgroup$– gung - Reinstate MonicaCommented Apr 5, 2017 at 16:59

Add a comment

|

1 Answer

$\begingroup$

$\endgroup$

I am not an expert but I would be happy to share my experience with the monomvn package.

Should I give initial values to beta?

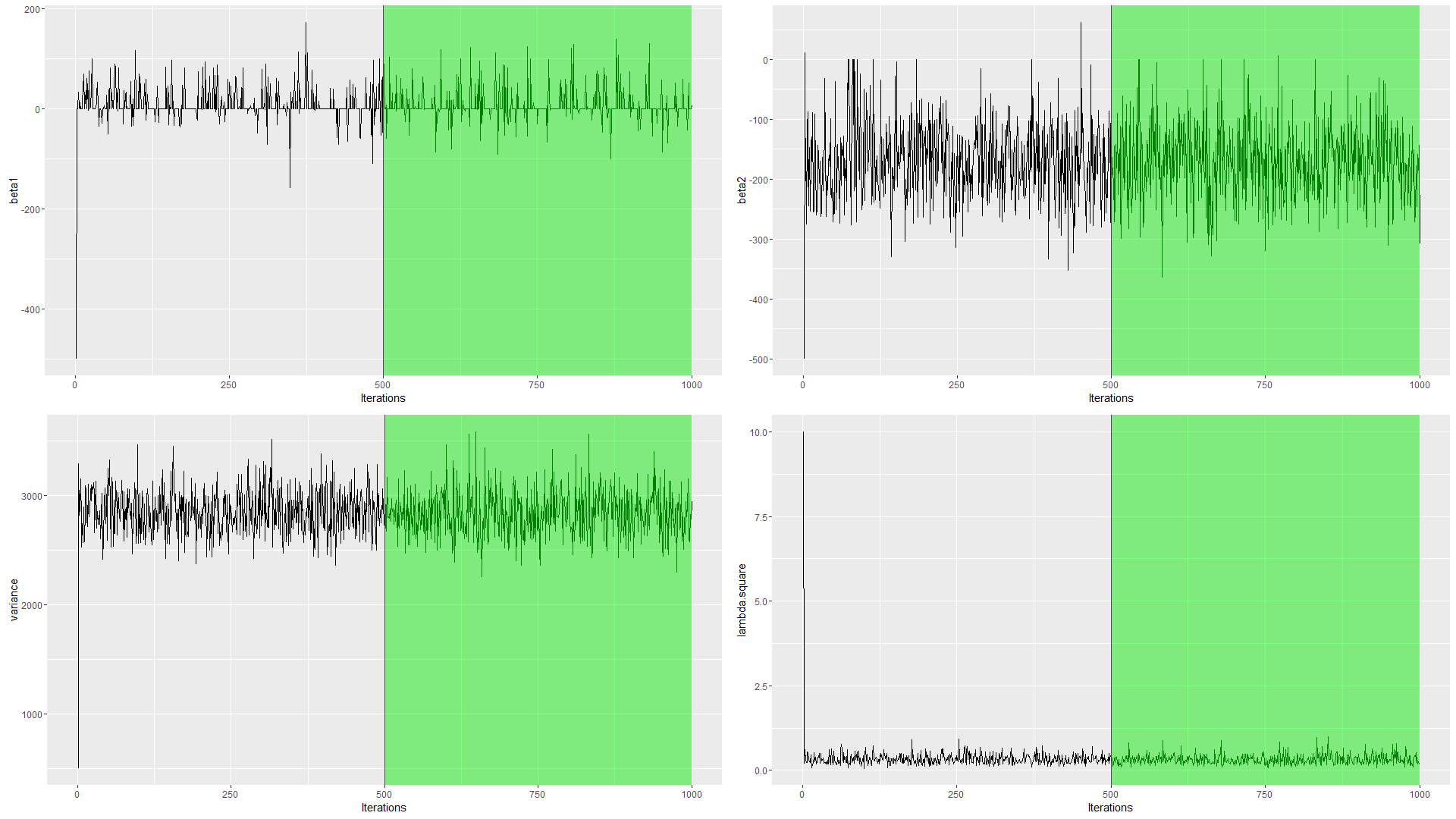

Given enough iterations, initial values shouldn't have any impact on any parameter (e.g. regression coefficients, error variance and penalty parameter). Please consider the R code and traceplots below:

# load required packages and datasets

library(monomvn); library(lars); library(glmnet); library(miscTools)

data(diabetes); attach(diabetes)

# define the burn-in period, number of mcmc samples to be drawn and initial values

burnin <- 500

iter <- 1000

initial.beta <- rep(-500, dim(x2)[2]) # assigning an extreme initial value for all betas

initial.lambda2 <- 10 # assigning an extreme initial value for lambda (penalty parameter)

initial.variance <- 500 # assigning an extreme initial value for variance parameter

# starting the Gibbs sampler here

lasso <- blasso(X = x2, # covariate matrix with dimensions 442 x 64

y = y, # response vector with length of 442

T = iter, # number of iterations

beta = initial.beta,

lambda2 = initial.lambda2,

s2 = initial.variance)

# collecting draws for some of the parameters for visualization

coef.lasso <- as.data.frame(cbind(iter = seq(iter),

beta1 = lasso$beta[, "b.1"],

beta2 = lasso$beta[, "b.2"],

variance = lasso$s2,

lambda.square = lasso$lambda2))

To get the parameter estimations, I would use the posterior median as Park and Casella (2008) have done.

> colMedians(coef.lasso[-seq(burnin), -1])

beta1 beta2 variance lambda.square

0.0000000 -172.3840906 2841.4410472 0.3031814

Please consider that I have computed the coefficients after discarding first half of the draws. Since I have considered only the draws from green-shaded areas, those extreme initial values I have assigned above have no impact on the posterior medians anymore.

I tried to follow this but when it comes to my data, all coefficients were shrunk to zeros.

Let's now compare lasso (glmnet package) and Bayesian lasso (monomvn package)

fit.glmnet <- glmnet(as.matrix(x2), y,

lambda=cv.glmnet(as.matrix(x2), y)$lambda.1se)

coef.glmnet <- coef(fit.glmnet)

sum(coef.glmnet == 0)

53

The original lasso implementation has shrunk 53 parameters to 0. Let's now check Bayesian lasso:

sum(colMedians(lasso$beta[-seq(burnin), ]) == 0)

56

and it shrank 56 out of 64 exactly to 0.

Please also note that your estimation results might significantly differ when you specify the prior distributions. A quick example would be to change the parameters using the 'rd' argument in blasso() where 'rd' controls the gamma prior on lambda^2. (please hit ?blasso for other hyperprior specifications)

Here is an example:

lasso2 <- blasso(X = x2, # covariate matrix with dimensions 442 x 64

y = y, # response vector with length of 442

T = iter, # number of iterations

beta = initial.beta,

lambda2 = initial.lambda2,

s2 = initial.variance,

rd = c(1, 1.78)) # hyperparameters suggested by Park & Casella (2008)

coef.lasso2 <- as.data.frame(cbind(iter = seq(iter),

beta1 = lasso2$beta[, "b.1"],

beta2 = lasso2$beta[, "b.2"],

variance = lasso2$s2, lambda.square =

lasso$lambda2))

colMedians(coef.lasso2[-seq(burnin), -1]) # new posterior median estimations

beta1 beta2 variance lambda.square

0.0000000 -183.7851178 2817.3811240 0.2313924

I hope it is now clear now that giving initial values doesn't really help. Have you tried estimating the parameters using glmnet? If the results differ a lot, then you might consider tuning the hyperpriors on parameters in blasso(). If you still get the same results, maybe the parameters are all indeed 0 :-)

Hope that helps!