I have the following multiple linear regression model:

Call:

lm(formula = Y ~ X1 + X2 + X2 + X3 + X4 + X5 + X6 + X7,

data = my.model, na.action = na.omit)

Residuals:

Min 1Q Median 3Q Max

-43.836 -1.507 0.010 1.485 46.231

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.0244927 0.0245157 -0.999 0.318

X1 -0.3484619 0.0134383 -25.931 <2e-16 ***

X2 0.1195273 0.0106940 11.177 <2e-16 ***

X3 0.1224587 0.0108849 11.250 <2e-16 ***

X4 -0.0010173 0.0028247 -0.360 0.719

X5 0.5496942 0.0156319 35.165 <2e-16 ***

X6 -0.2287941 0.0145018 -15.777 <2e-16 ***

X7 -0.2315801 0.0146361 -15.823 <2e-16 ***

X8 0.0005465 0.0003595 1.520 0.128

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 2.936 on 35849 degrees of freedom

(12534 observations deleted due to missingness)

Multiple R-squared: 0.05968, Adjusted R-squared: 0.05947

F-statistic: 284.4 on 8 and 35849 DF, p-value: < 2.2e-16

The model is affected by multicollinearity but my question is about the forecast, so this shouldn't be an issue.

I checked the absolute values of my model forecast and compared against the actual Y absolute values. The average of the absolute predicted values is significantly lower than the absolute observed values mean:

> lm1.predict = predict(lm1, mydata)

> mean(abs(lm1.predict))

[1] 0.3294776

> mean(abs(mydata$Y))

[1] 1.206954

Does this mean that the linear regression variables I am using tend to underestimate the outcomes? Can any other conclusion be derived from this simple comparison?

EDIT

Another way to look at this is to calculate the absolute difference between each observation and the relative outcome:

> mean(abs(mydata$Y - lm1.predict))

[1] 1.208378

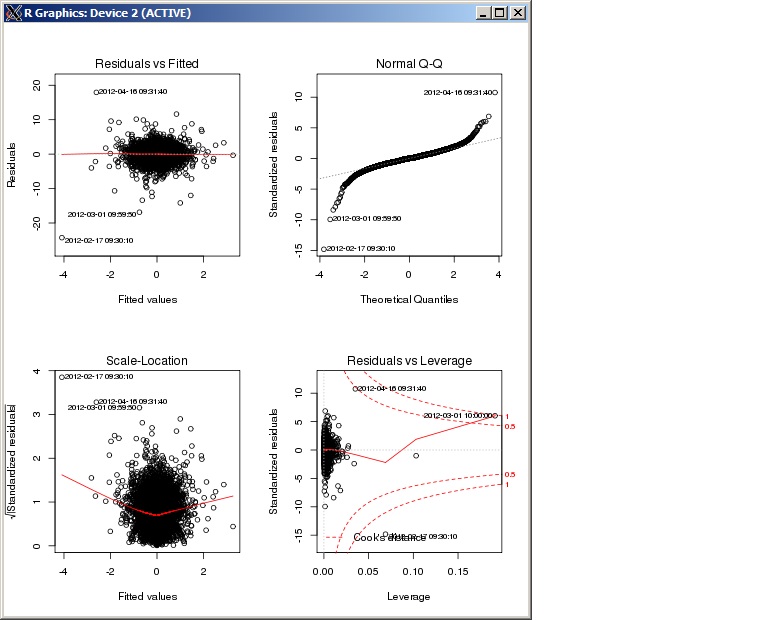

These are the diagnostic from the regression: