I know that $\int_{0}^{\infty} 1-F(t) dt$ is the expectation of a random variable. But what happens when the upper limit is some finite number like so? \begin{align*} \int_{0}^{x} 1-F(t) dt \end{align*} where F is the CDF of a gamma distribution and $F(x)<1$. What's the interpretation? Are there any other, more intuitive, forms to represent this?

I tried to understand the meaning by calculating the above for Uniform[0,1] distribution over interval [0,1/2] which resulted in 1/8. But it still isn't intuitive.

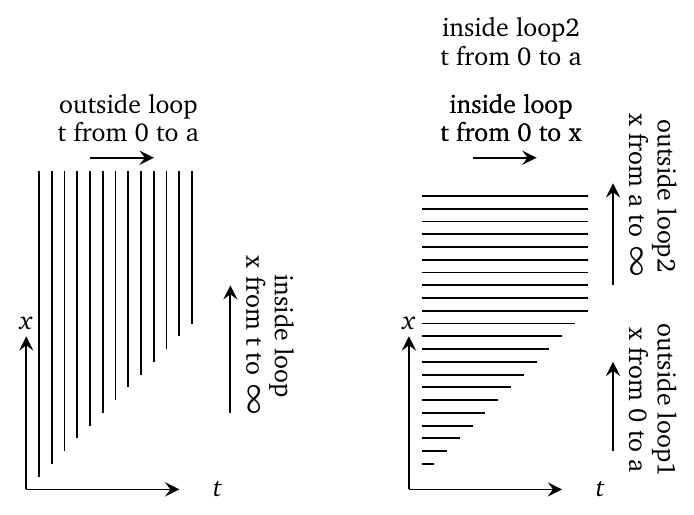

For another form, I started doing similar derivation to the one here: Firefeather's answer to Find expected value using cdf, hoping that it would somehow simplify my integral but that led me to no better place. I end up with the following \begin{align*} \int_{0}^{x} 1-F(t) dt &= \int_{0}^{x} Pr(T>t) dt \\ &= \int_{0}^{x}\int_{t}^{\infty}f(y) dy dt \\ &= \int_{0}^{\infty}\int_{0}^{Min(y,x)}f(y) dt dy \\ &= \int_{0}^{\infty}Min(y,x)f(y) dy \\ & =\int_{0}^{x}yf(y) dy + \int_{x}^{\infty}xf(y) dy \\ \end{align*} There's still no intuition/interpretation.

Finally, in special case of Erlang distribution, since it results from adding a bunch of exponentially distributed random variables, I thought that maybe I need to look into renewal functions from stochastic processes to get a better understanding of the above integral but no success so far.