As I understand it, one can model changing variance of a time series process with a GARCH model. What I don't understand is, how can one actually make predictions with this?

Since

$$

y_t = \sigma_t \epsilon_t

$$

with $\epsilon_t$ being a Gauss-distributed random variable, the expected value of this is always zero. So how does it help to know, how big the variance is, when both an up and a down are equally likely?

Or did I understand something wrong?

$\begingroup$

$\endgroup$

3

-

$\begingroup$ Ok, so it is also not used in combination with for example ARIMA, to give better predictions? $\endgroup$– Luca ThiedeCommented Nov 20, 2017 at 20:20

-

$\begingroup$ Check out existing questions on GARCH models; perhaps your question has already been answered. See e.g. this or these. Actually, I am pretty sure there has been at least one question which is either very similar or the same as yours. $\endgroup$– Richard HardyCommented Nov 20, 2017 at 20:22

-

$\begingroup$ See also this and this which may be helpful. $\endgroup$– Richard HardyCommented Nov 20, 2017 at 20:31

Add a comment

|

1 Answer

$\begingroup$

$\endgroup$

3

GARCH can be used for what you call predictions. The question is: predictions of what? Predictions of volatility.

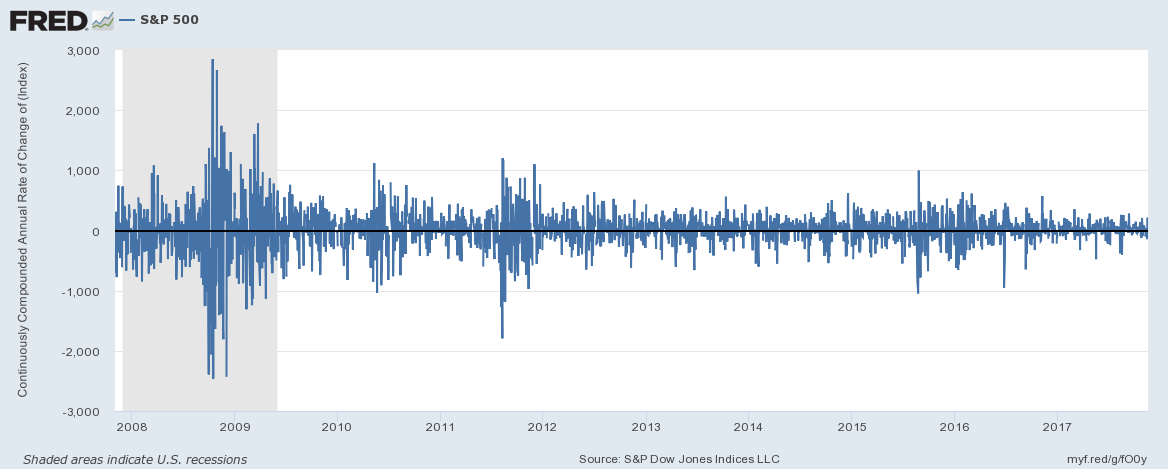

The reason why GARCH is useful is because it may better explain the volatility of certain series, particularly in finance. For instance, look at the graph below. It shows daily log differences of S&P 500 series. Clearly, the volatility is lower lately than it was a few years ago, and moreover it seems to be clustered. Notice, the bursts of high volatility.

This kind of series is not well explained by a standard random walk series where the variance is constant. Therefore, we have more complicated models such as GARCH that seem to explain the volatility better, and where volatility is not constant.

Estimation of volatility is very important in risk management and option pricing. We may not have a good predictor of where the prices go, but it doesn't prevent us from assessing of risks of holding these assets and valuing them.

-

$\begingroup$ FYI, the question is surely a duplicate, someone just needs to dig down the pile of older questions to find it. Hence better answer the original one than this one. $\endgroup$ Commented Nov 20, 2017 at 20:28

-

$\begingroup$ @RichardHardy I dont recall anyone asking it this way, why is GARCH useful $\endgroup$– AksakalCommented Nov 20, 2017 at 20:31

-

4$\begingroup$ Having answered nearly a couple hundreds of GARCH questions on this site, I do recall a few in this vein, but digging through 189 answers is hard :) $\endgroup$ Commented Nov 20, 2017 at 20:32