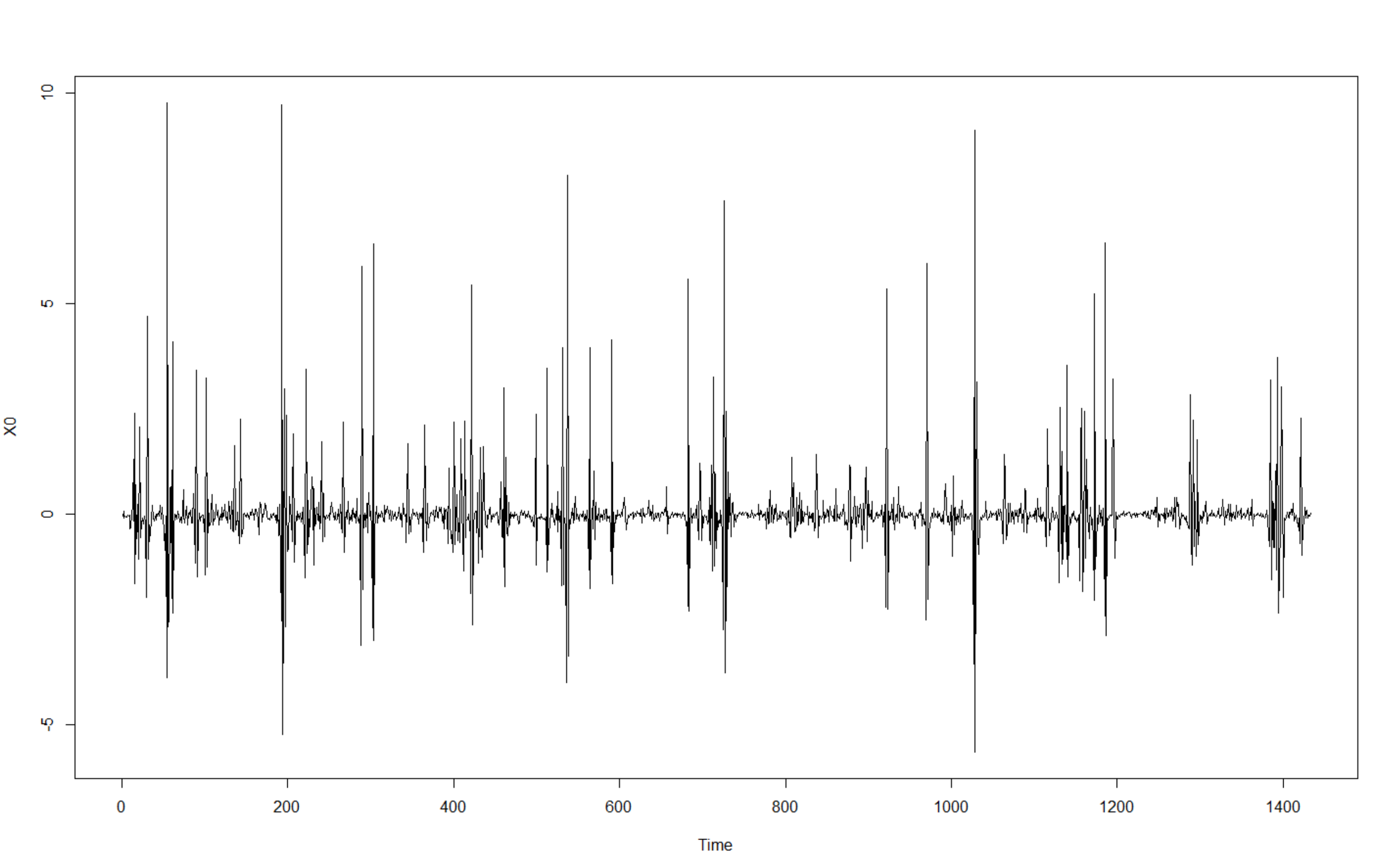

I've been working on fitting a time series generated from an indicator in stock market, whose frequency is 1 minute and length is 1433. This series is stationary, proved by many stationarity tests. The graph of this series lies below.

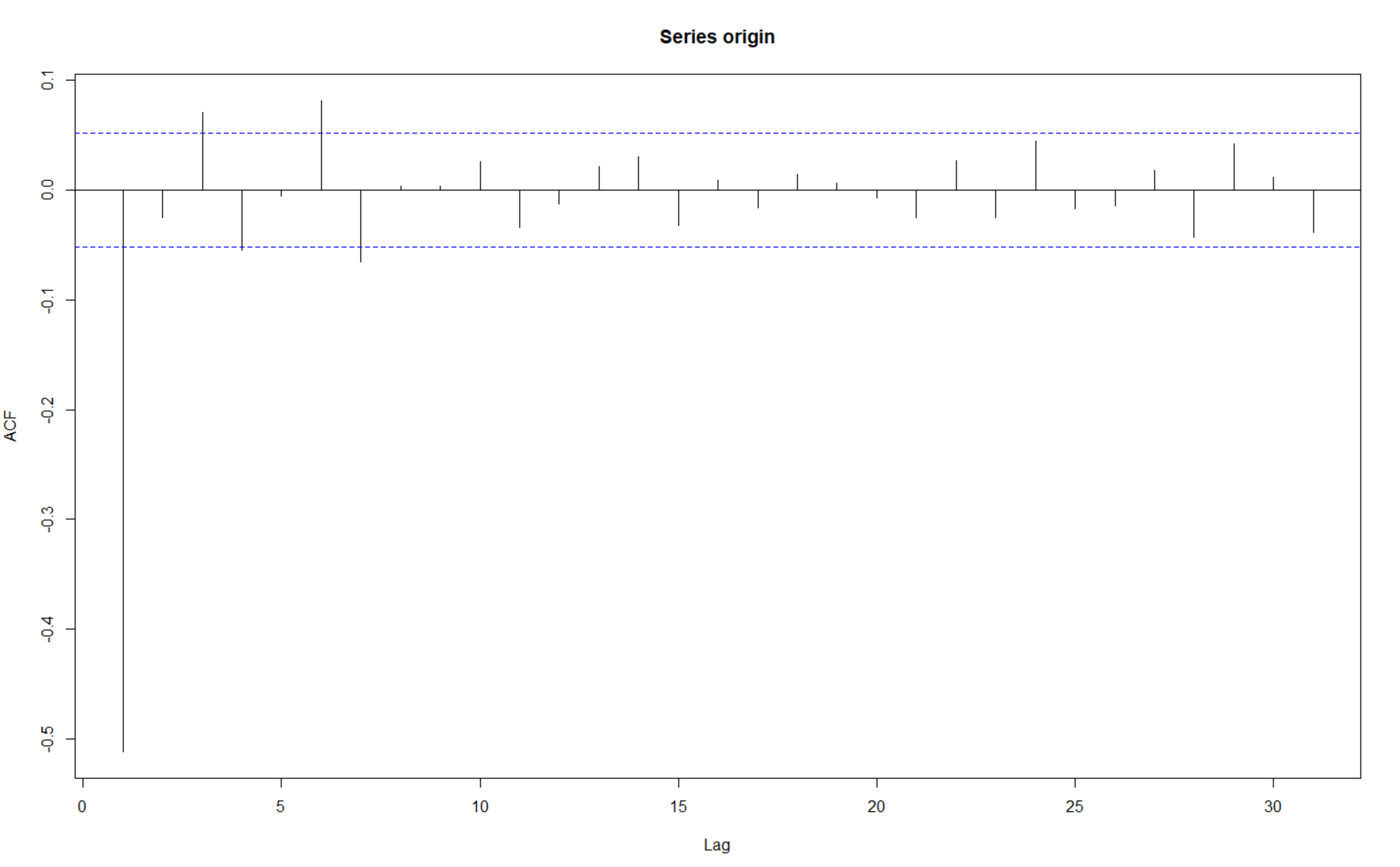

However, I faced great difficulty fitting this time series, though it passed neither Ljung-Box test nor Box-Pierce test, and its autocorrelation is indicated by the graph below.

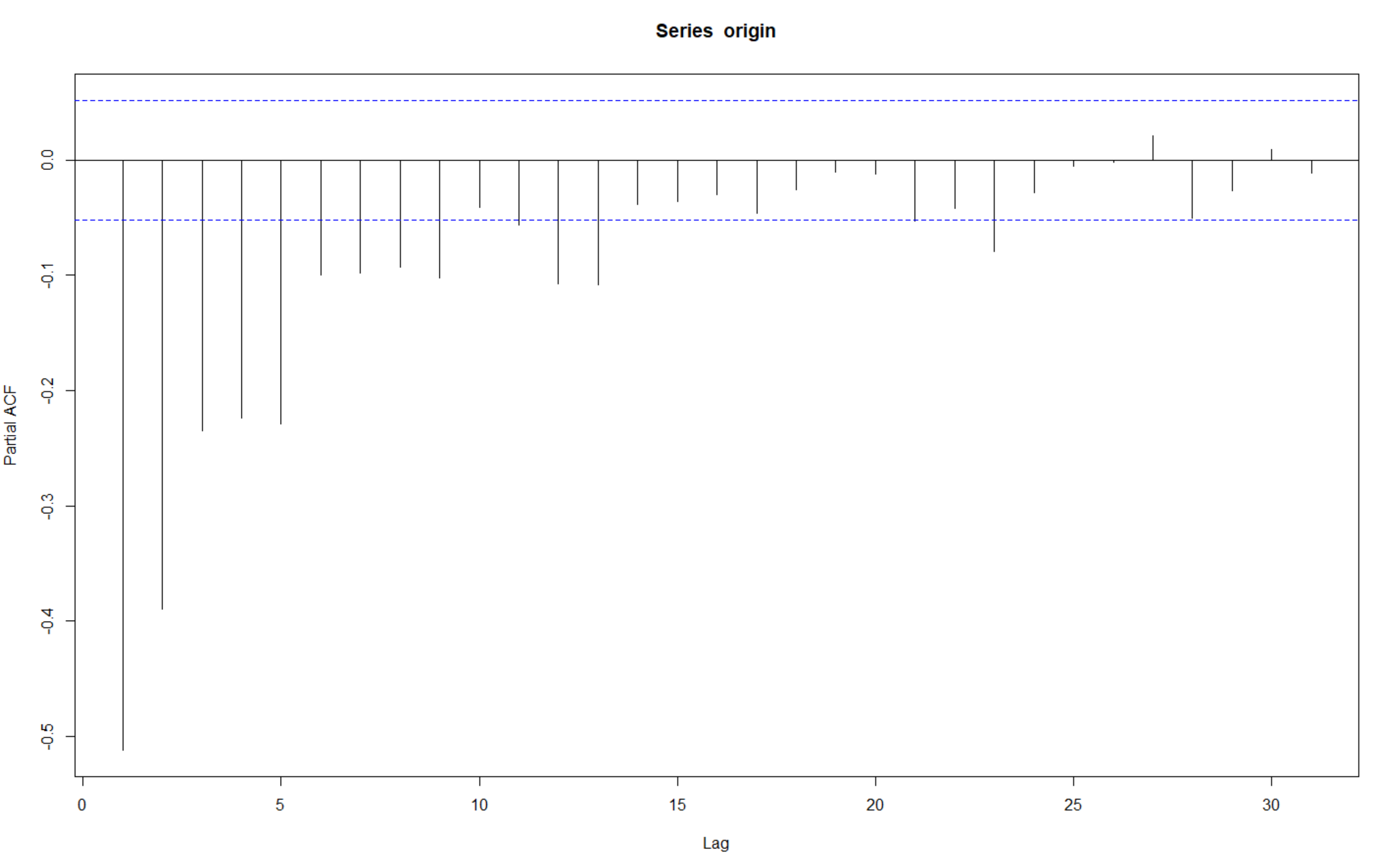

And its partial autocorrelation is like this.

I've tried to fit this time series by ARIMA, whose arguments were chosen by both EACF and iterative process finding the suitable AIC. but the results were not pleasant at all.

I also made attempt by using Kalman filter. Since I haven't learnt much on state space model, I tuned the parameters due to my intuition and the mathematical logic beneath the series. The result was good...But then I got stuck when trying to forecast the series 1-step afterwards without observation...

I wonder if there is anyone who can help me on this issue... Many thanks since it has troubled me for a long time...