I have fitted a DCC GARCH model to my multivariate financial returns data. Now, I need to compute the time-varying conditional correlation matrix by using the standardized residuals obtained from the DCC-GARCH estimation. Here, the problem is I do not know how to compute conditional correlation matrix by using standardized residuals.

Below is my reproducible code:

load libraries

library(rugarch)

library(rmgarch)

data(dji30retw)

Dat = dji30retw[, 1:8, drop = FALSE]

uspec = ugarchspec(mean.model = list(armaOrder = c(0,0)), variance.model = list(garchOrder = c(1,1), model = "eGARCH"), distribution.model = "norm")

spec1 = dccspec(uspec = multispec(replicate(8, uspec)), dccOrder = c(1,1), distribution = "mvnorm")

fit1 = dccfit(spec1, data = Dat)

print(fit1)

My question: Is it possible to obtain the time-varying conditional correlation matrix as well as variance of the returns, by using standardized residuals obtained from the DCC-GARCH estimation? I have tried the following code without residuals, but not sure whether it is correct or not:

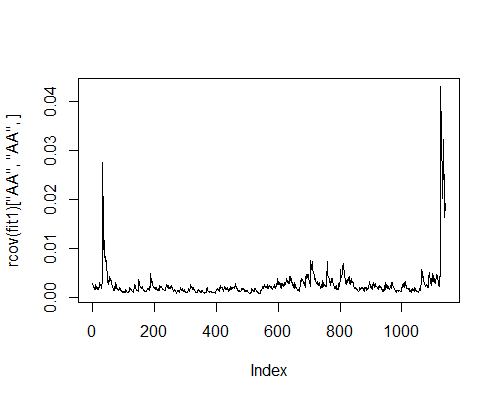

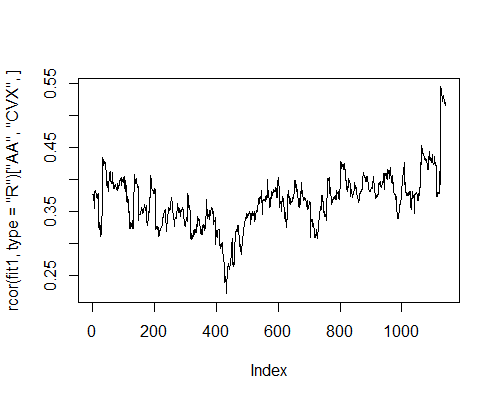

r1=rcor(fit1, type="cor")

Kindly help me to get the time-varying correlation matrix by using the standardized residuals. I also need help to obtain the variances of each individual returns.

A kind help will be highly appreciated.

Thanks in advance.