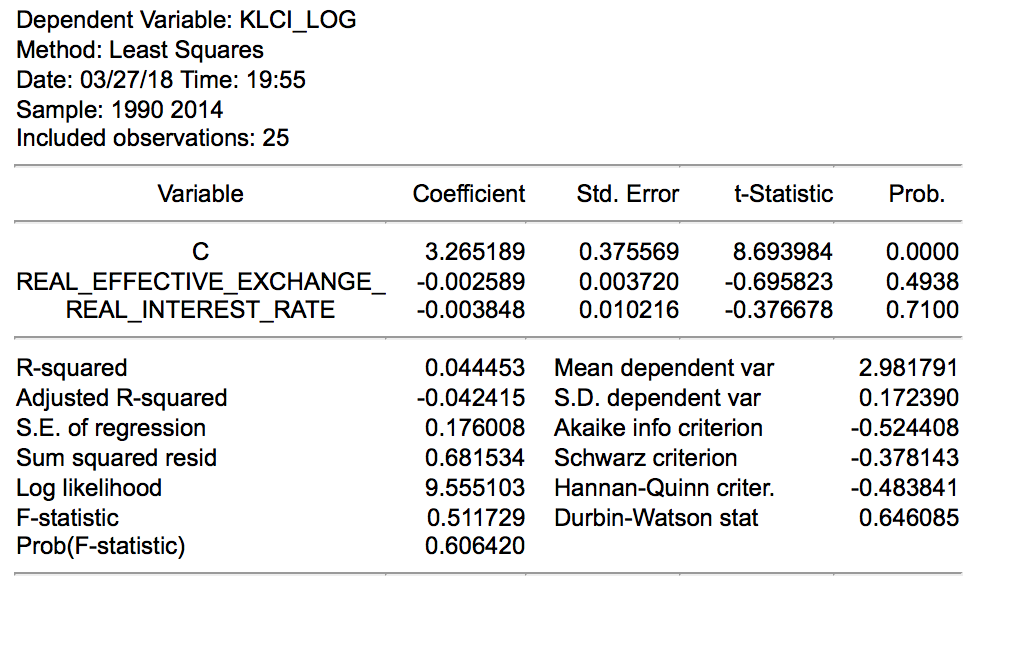

I've conducted ols regression analysis on stock market index KLCI (dependent) and 2 other independent variables that includes exchange rate (ER) and interest rate (IR). And the result shows that i have 0.044 for r-sqaured while -0.042 for adjusted r-squared. By looking at the result, my lecturer told me that the model is not capturing my dependent variable. i've collected 25 annual data each on the stock market index, real interest rate and the real effective exchange rate on conducting it.

How do i need to adjust the data to be able to have a proper regression results? I used log(KLCI) c ER IR on Eviews.