Hi I am new to time series and I got this problem. At first I created a simple seasonal ARIMA model using auto.arima and forecast library.

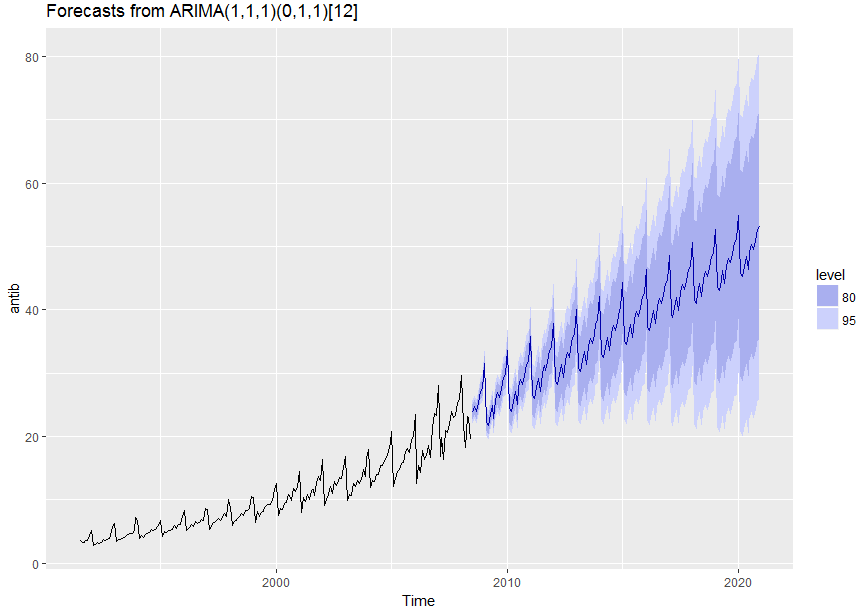

Then when I tried to make prediction using this model, variance always remained constant. It shouldnt be like that, when you look at train data, variance should be growing. Because of growing trend. (I tried this on other datasets and result was the same)

What should I do? How to change this model, to get rid of constant variance? :(

Thanks.

Code:

antib = a10

model = auto.arima(antib, stationary = FALSE)

prediction = forecast(model, h = 150)

autoplot(prediction)