One possible reason you can get high AUROC with what some might consider a mediocre prediction is if you have imbalanced data (in favor of the "zero" prediction), high recall, and low precision. That is, you're predicting most of the ones at the higher end of your prediction probabilities, but most of the outcomes at the higher end of your prediction probabilities are still zero. This is because the ROC score still gets most of its "lift" at the early part of the plot, i.e., for only a small fraction of the zero-predictions.

For example, if 5% of the test set are "ones" and all of the ones appear in the top 10% of your predictions, then your AUC will be at least 18/19 because, after 18/19 of the zeroes are predicted, already 100% of the ones were predicted. Even if the top 5% are all zeroes.

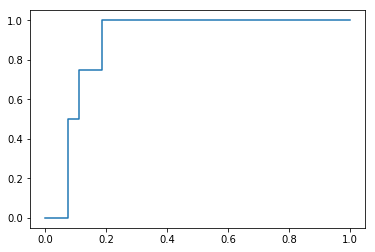

A simple python example:

import sklearn

import numpy as np

yTest = [0,0,1,1,0,1,0,0,1,0,0,0,0,0,0,0,0,0,0,0,0,0,0,0,0,0,0,0,0,0,0]

yPredicted = np.linspace(0.9, 0.1, num=len(yTest))

sklearn.metrics.roc_auc_score(yTest, yPredicted) # ~0.89

import matplotlib.pyplot as plt

fpr, tpr, threshold = sklearn.metrics.roc_curve(yTest, yPredicted)

plt.plot(fpr, tpr)

Whether this is a "bad" prediction depends on your priorities. If you think that false negatives are terrible and false positives are tolerable, then this prediction is okay. But if it's the opposite, then this prediction is pretty bad.

A common real world scenario where this happens is when you include samples that are "out-of-scope" in your model, and your model correctly identifies that all those samples have ~0% chance of having target=1.

For example, suppose you are predicting the probability of a transit employee getting into a vehicle collision, and you use, as a predictor, a categorical variable "job type" which has values "bus driver", "ticket booth operator", and "fare enforcer". Your model will identify that the booth operators and fare enforcers have ~0% chance of a crash, putting them all at the tail end of your predictions and increasing the concentrations of 1s at the top, inflating your AUC. However, the business folks who commissioned this model would know that those job types are obviously not candidates, and if you asked them, they would tell you not to include those samples in the scope of your model. Adding the obvious out-of-scope samples artificially inflated your AUC. (This has happened to me multiple times, where my "first pass" of a model gave me an AUC >98% making me think I'm a rockstar, until I trimmed down the scope and then observed a more sobering score.)