First, how would I accomplish the second approach (would I be sampling from a multivariate normal distribution)?

You can indeed do this by sampling from a multivariate normal distribution. If you are using R for your simulations then you can sample using the mvrnorm function in the MASS package. Here is an example where I have generated a large number of simulated values using a given mean vector and variance matrix:

set.seed(1);

#Create example of mean vector and variance matrix

#Checked eigenvalues to ensure it is a valid variance matrix

M <- matrix(c(16, 17, 14), ncol = 1);

V <- matrix(c(3.2, 1.1, 1.5, 1.1, 4.8, 2.1, 1.5, 2.1, 6.0), ncol = 3);

#Generate n values from normal distribution with above mean and variance

library(MASS);

n <- 10^5;

SIM1 <- mvrnorm(n, mu = M, Sigma = V);

Alternatively, you can also generate independent standard normal random variables and transform them so that they come from the desired multivariate normal distribution:

#Find principal square root of variance matrix

SS <- diag(eigen(V)$value);

EE <- eigen(V)$vectors;

S <- EE %*% sqrt(SS) %*% t(EE);

#Generate n values from normal distribution with above mean and variance

SIMB <- matrix(0, nrow = n, ncol = 3);

for (i in 1:n) { SIMB[i,] <- t(M + S %*% rnorm(3,0,1)); }

Second, are these two approaches equivalent as long as I assume that the weights W of my portfolio remain the same?

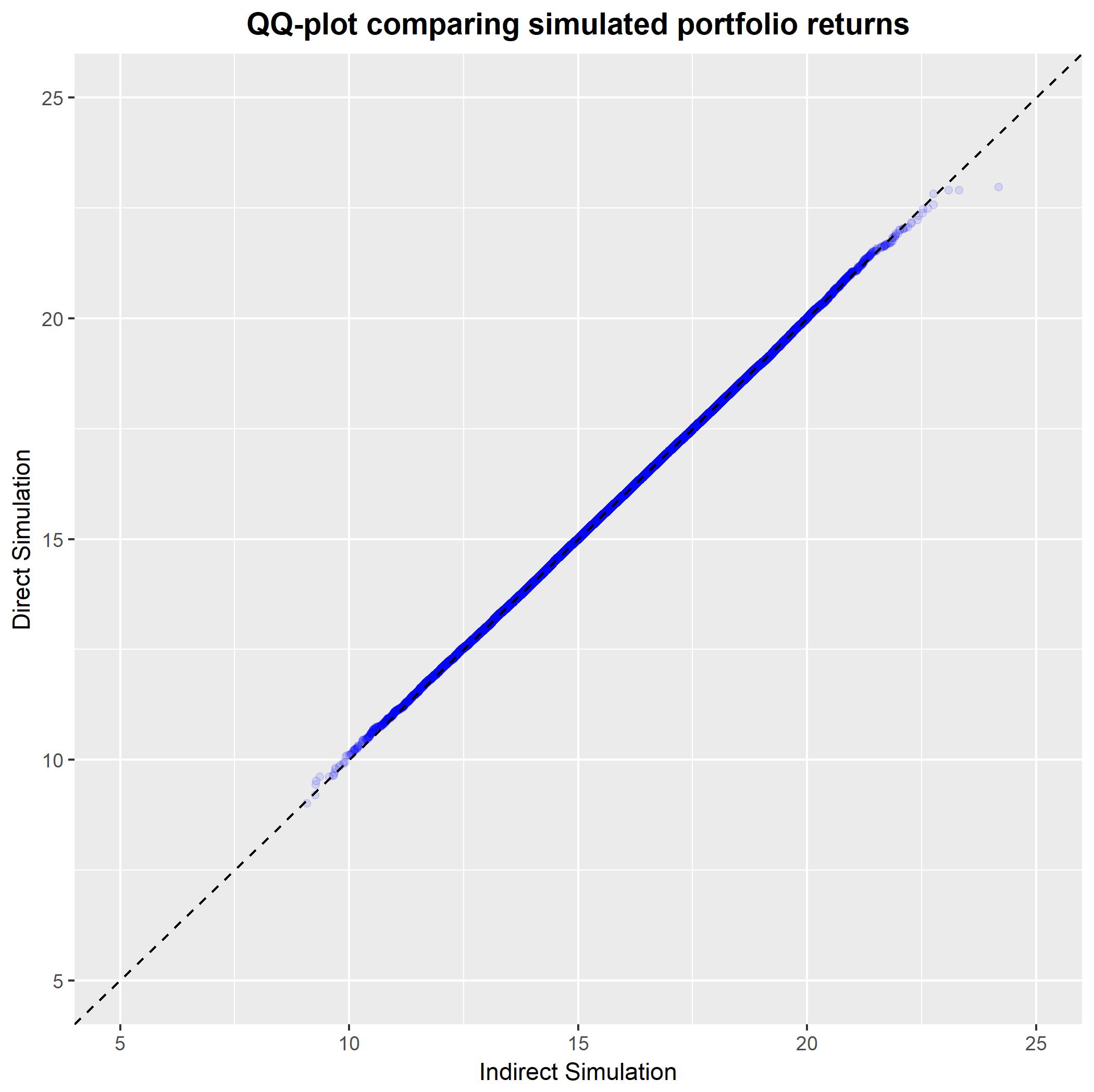

Yes, they are the same. Your derivation of the distribution of your portfolio return is correct, and so the two simulations should yield values from the same distribution. To confirm this, let's go ahead and simulate using the direct method and then generate a QQ-plot to confirm that both methods give values from the same distribution:

#Create example weights

W <- c(0.2, 0.5, 0.3);

#Generate values for portfolio return via indirect method

VALS1 <- rep(0, n);

for (i in 1:n) { VALS1[i] <- sum(W*SIM1[i,]) }

#Generate values for portfolio return via direct method

MP <- sum(W*M);

VP <- t(W) %*% V %*% W;

VALS2 <- rnorm(n, mean = MP, sd = sqrt(VP));

#Create QQ-plot comparing values

plot(sort(VALS1), sort(VALS2),

main = 'QQ-plot comparing simulated portfolio returns',

xlab = 'Indirect Simulation', ylab = 'Direct Simulation');

abline(a = 0, b = 1, lty = 3);

ggplot(data = data.frame(x = sort(VALS1), y = sort(VALS2)),

aes(x = x, y = y)) +

geom_point(alpha = 0.1, colour = 'blue') +

geom_abline(intercept = 0, slope = 1, linetype = 'dashed') +

scale_x_continuous(limits = c(5,25)) +

scale_y_continuous(limits = c(5,25)) +

theme(plot.title = element_text(hjust = 0.5, size = 14, face = 'bold')) +

ggtitle('QQ-plot comparing simulated portfolio returns') +

xlab('Indirect Simulation') + ylab('Direct Simulation');