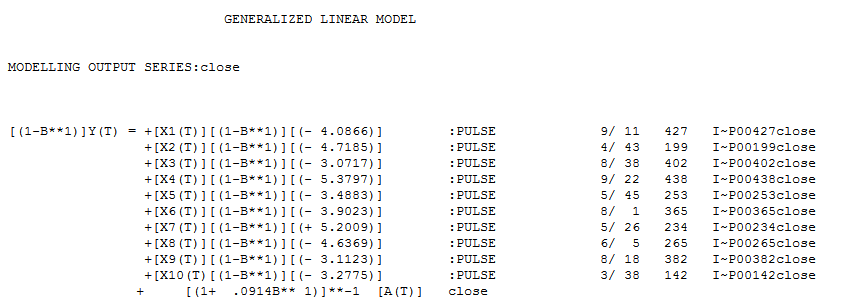

I'm trying to employ an ARIMA model, and have run into the following conundrum:

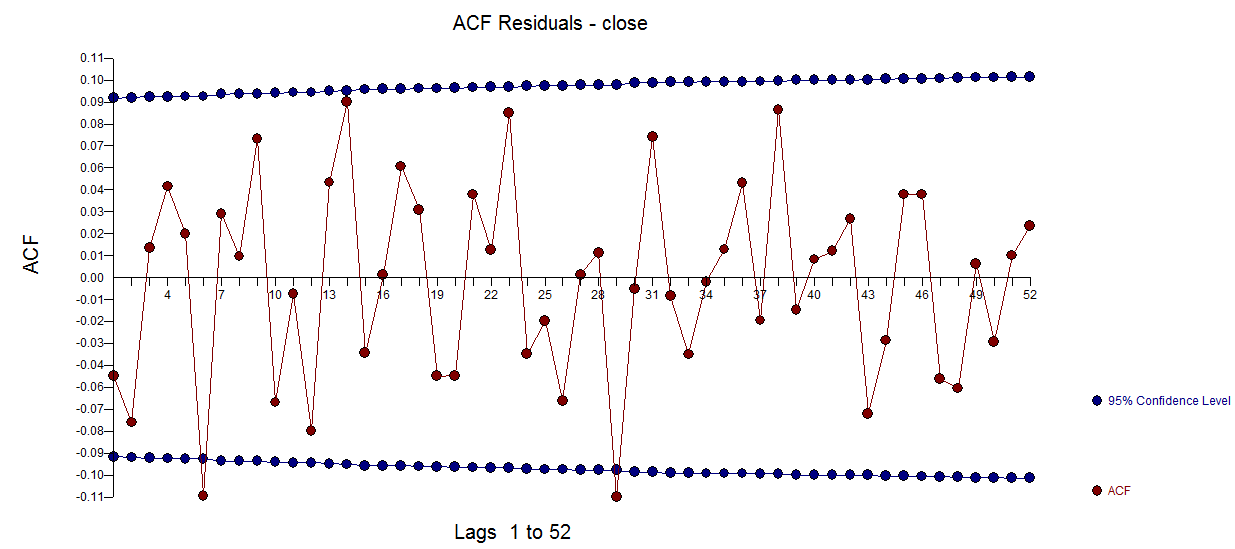

when I employ differencing or other transforms to successfully achieve stationarity (at least according to the Augmented Dickey Fuller Test), my ACF/PACF plots are ambiguous at best:

...yet only when I employ a transform that does not achieve stationarity via Dickey Fuller standards (sub-optimal p values of 1-3) am I actually able to obtain typical ACF/PACF plots that could yield the order of my model.

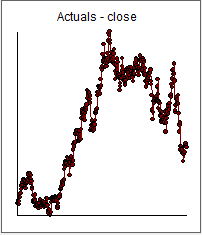

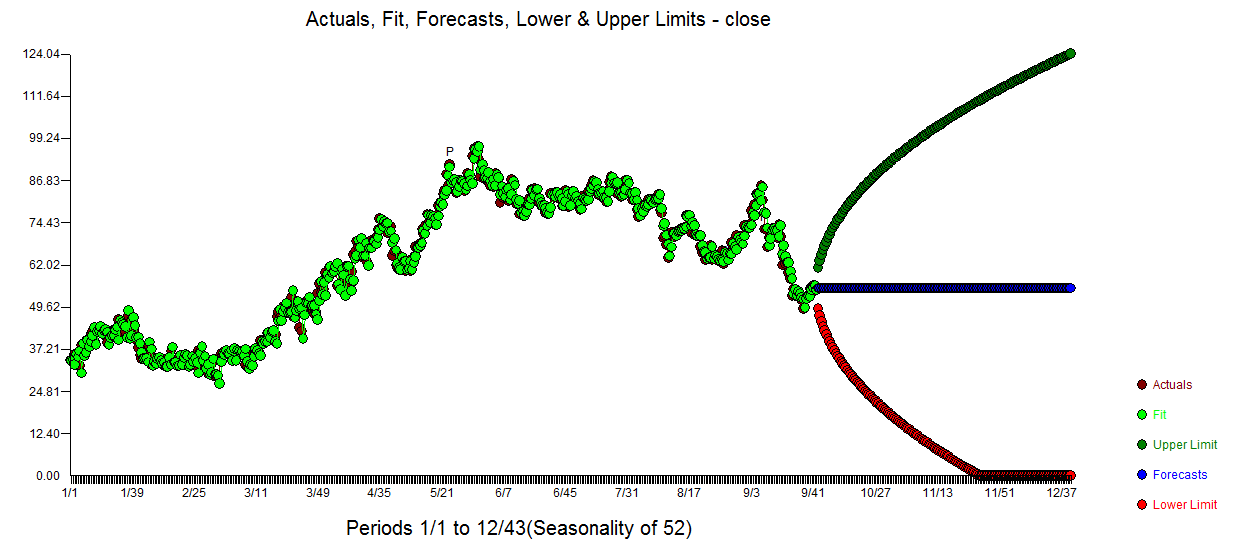

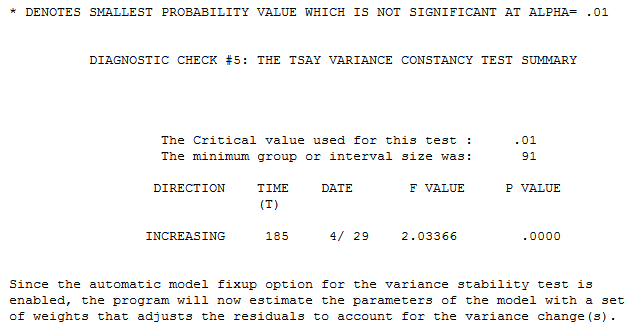

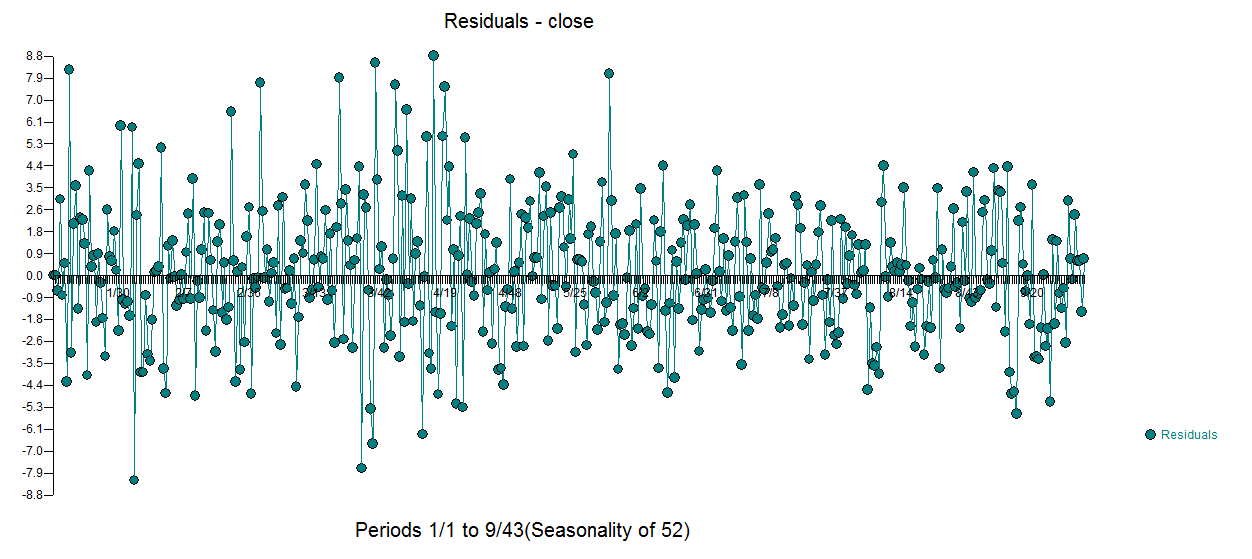

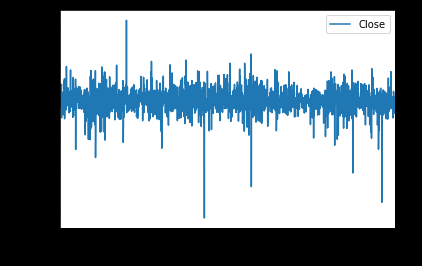

Knowing that Dickey Fuller can only test stationarity with regards to trend (and not variance and other factors), I'm left to wonder if the problem is that my data isn't as stationary as indicated by that test. As you will see from the plot, there are certain considerable outliers, so I considered that they were the root of the problem:

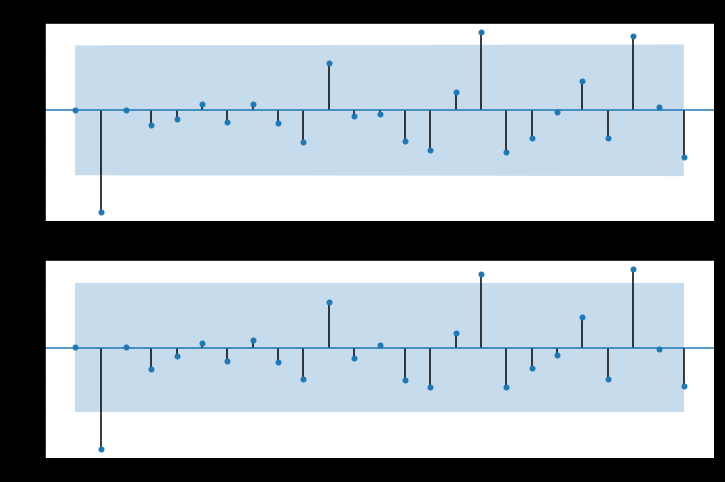

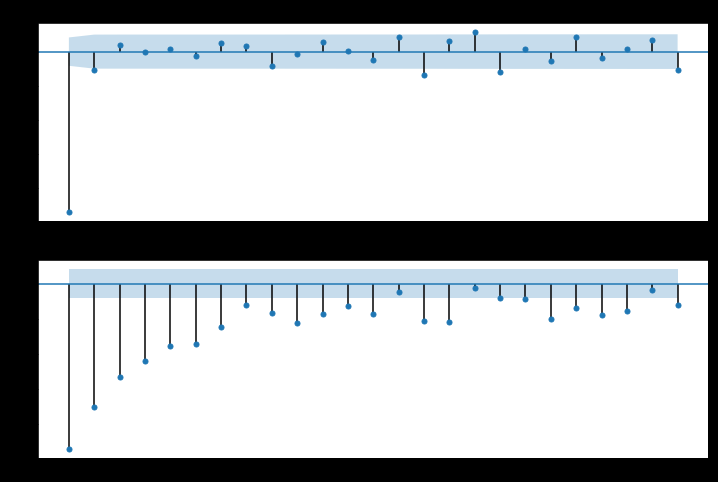

Yet even after dealing with these outliers in a variety of ways, and improving stationarity as reflected by Dickey Fuller (and a more stationary-looking plot), my ACF/PACF plots remain just as ambiguous as shown in the first figure. I have tried many means of differencing and transforming, but with the same result. Is lack of stationarity still the likely problem? Or is it something else I'm not considering, and if so, what? Thank you in advance.

My data (weekly price data going back to November 2010) can be found here: https://www.dropbox.com/s/gl3irup6csygctf/WBAWeekly.csv?dl=0