I have a weekly series stored in a tsibble called data:

data

# A tsibble: 50 x 2 [1W]

Yw Series

<week> <dbl>

1 2018 W26 0.352

2 2018 W27 0.457

3 2018 W28 0.435

4 2018 W29 0.106

5 2018 W30 0.188

6 2018 W31 0.226

7 2018 W32 0.0769

8 2018 W33 0.359

9 2018 W34 0.194

10 2018 W35 0.1

# … with 40 more rows

Using forecast::auto.arima() this is what I get:

> auto.arima(data$Series) %>% summary()

Series: data$Series

ARIMA(0,1,1)

Coefficients:

ma1

-0.8024

s.e. 0.1175

sigma^2 estimated as 0.01157: log likelihood=39.72

AIC=-75.43 AICc=-75.17 BIC=-71.65

Training set error measures:

ME RMSE MAE MPE MAPE MASE ACF1

Training set -0.01972258 0.1053875 0.08478854 -37.38673 56.40025 0.8320206 0.1053078

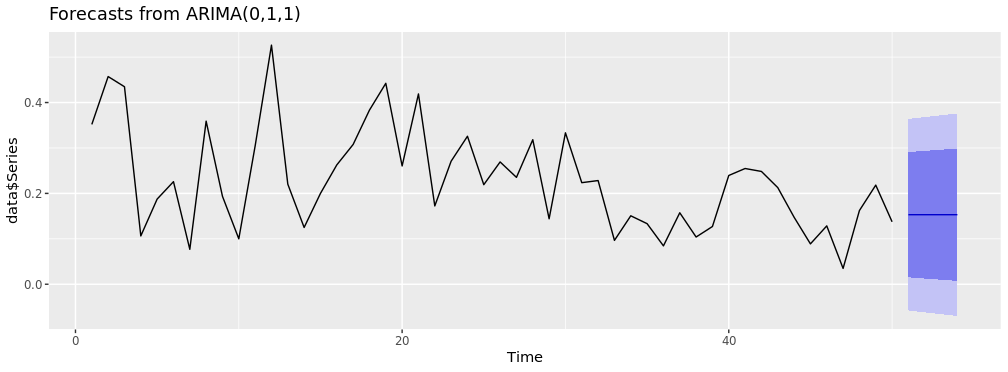

I want to forecast the series for the next month, and it's weekly data, so I ran:

auto.arima(data$Series) %>%

forecast::forecast(h = 4) %>%

autoplot()

And this is what I get:

Point Forecast Lo 80 Hi 80 Lo 95 Hi 95

51 0.1530928 0.015248242 0.2909373 -0.05772223 0.3639077

52 0.1530928 0.012584137 0.2936014 -0.06179663 0.3679821

53 0.1530928 0.009969614 0.2962159 -0.06579520 0.3719807

54 0.1530928 0.007402002 0.2987835 -0.06972202 0.3759075

This seems so strange to me. The point estimate is the same for all four weeks ahead and there's no autoregressive component in the model. I've checked and ARIMA(0,1,1) beats all other specifications on both AIC, AICc and BIC.

Can anyone shed some light on this?

auto.arimawould select such a model? $\endgroup$