I'm trying to understand the "Combinatorial Purged Cross-Validation" technique for time series data described in Marcos Lopez de Prado's "Advances in Financial Machine Learning" book (p. 163).

The setup is described as the researcher wanting to test "a number $\phi$ of backtest paths." I'm not really sure what that means, but here's what I have so far:

- A time series is split into $N$ sequential groups

- A number $k$ is chosen for cross validation

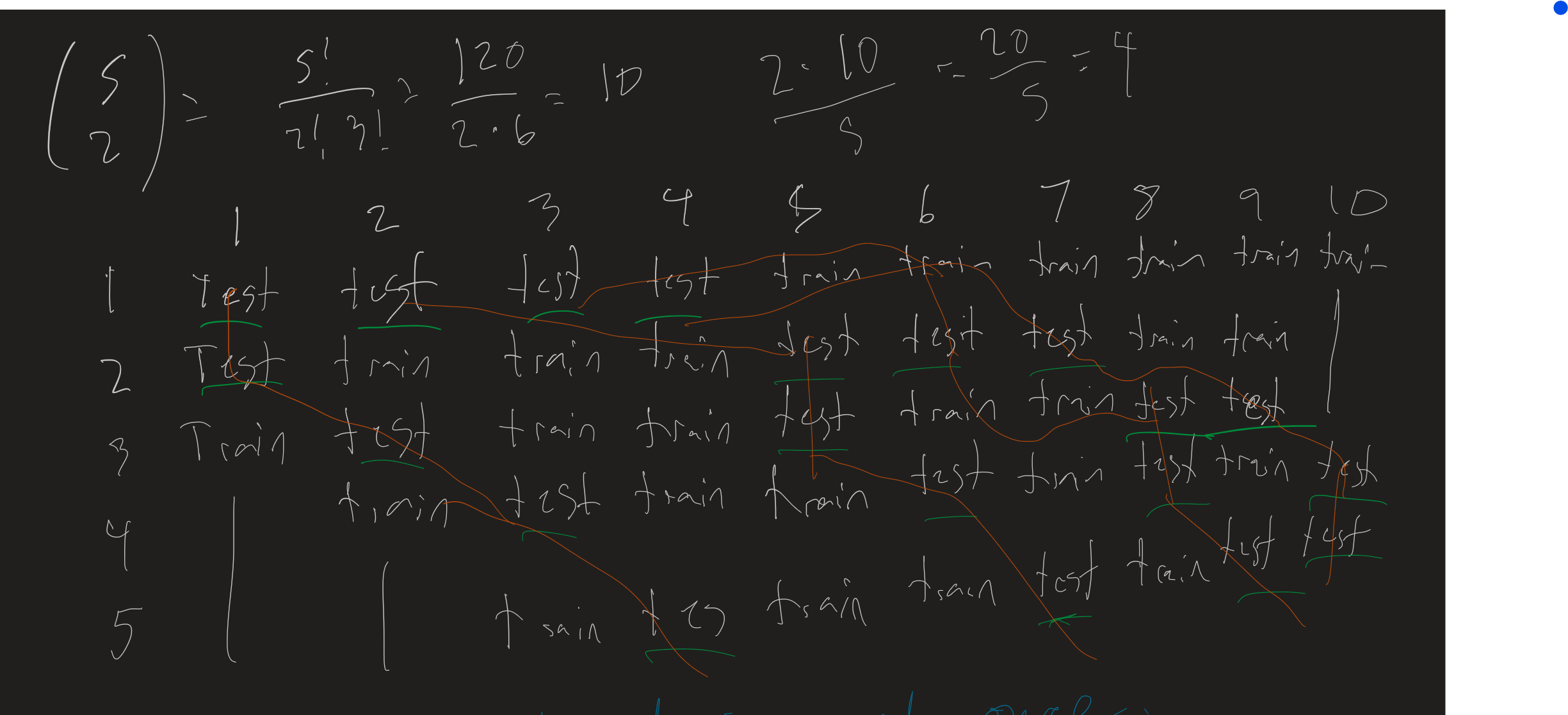

- A combinatoric equation is used to calculate the "number of paths": $$ \phi(N, k) = \frac{k}{N}{N \choose N - k}. $$

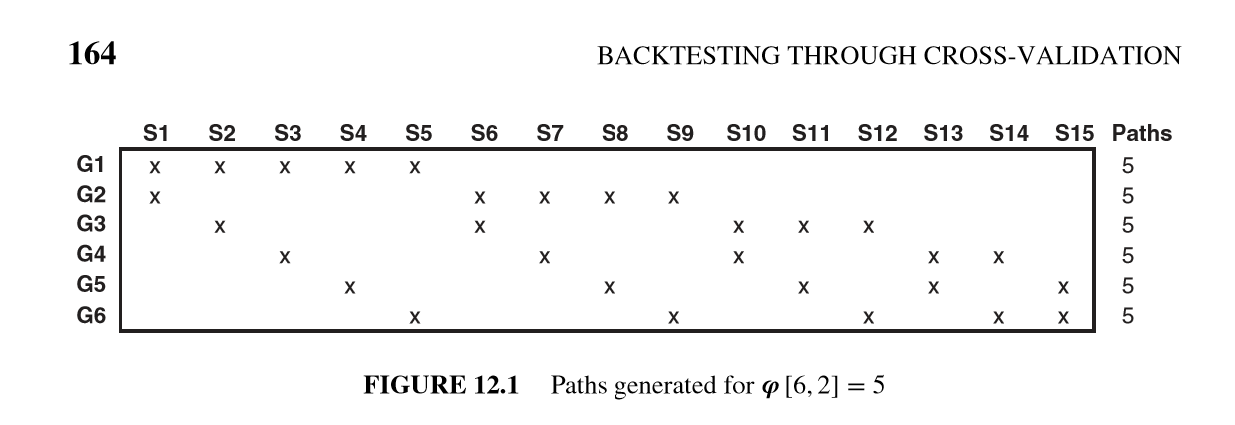

For the case of $N=6$ groups and $k=2$, there are $\phi(6, 2)=5$ paths and Figure 12.1 from the book lays them out as a table. The number of train / test CV split" is 15 (6 choose 2), which are indexed as the columns in the table below. The rows are the 6 groups, and the numbers inside are the path ids from 1 to 5.

The book states, "Path 2 is the result of combining forecasts from (G1,S2), (G2,S6), (G3,S6), (G4,S7), (G5,S8) and (G6,S9)." The passage of time through the G-groups, I can see. What I'm not following is how the splits relate to the groups.

People obviously think highly of this book. Here's a video of someone explaining Combinatorial Purged Cross Validation, but it didn't answer my questions. Can anybody tell me what's going on here? Is this truly an advancement over Walk Forward Cross Validation?