Can anyone help me out with this question I found on my practice paper?

The series $\{y_t\}$ is described by

$$ y_t = 5+0.3y_{t-1}+\epsilon_t+0.9\epsilon_{t-1}. $$

Identify the specific ARIMA model. What is the mean of the series $\{y_t\}$?

I think it is a ARMA (1,1) process? is that correct? And how do I calculate the mean of the ARMA model? Is it the same as AR model? If it is then

$$ E(y_t) = 5/ (1-0.30) = 7.14?$$

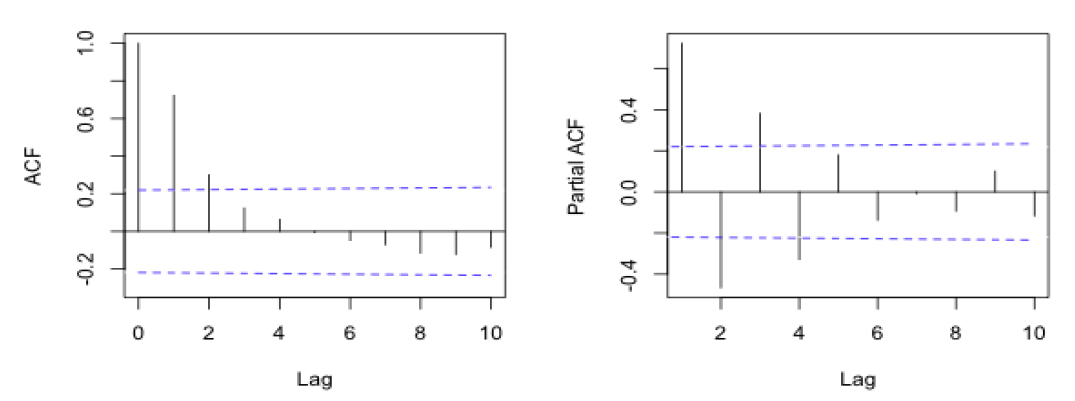

The sample ACF and PACF plot of a series are given above. Appraise the patterns and judge which ARIMA model fit the series. Justify your conclusion.

I identified as the AR(4). Is that correct? Since ACF has an exponential decay and PACF has a cut off? Differencing is not needed as the ACF decreases sufficiently to 0.