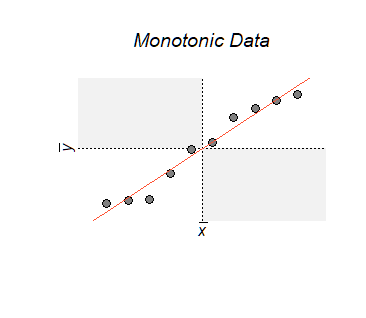

In the scatterplot of any $(x,y)$ data, the least squares fit (red line in the figure) will pass through the point of averages $(\bar x,\bar y),$ located at the intersection of the dotted axes.

When the relationship is monotonic, all the points lie in the unshaded quadrants. This means that to the left of the point of averages all the $x_i$ are less than $\bar x$ and monotonicity implies all the $y_i-\bar y$ in that region have the same sign. To the right of the point of averages all the $x_i-\bar x$ are positive but the signs of all the $y_i-\bar y$ are the opposite of what they were to the left. Unless these data lie on a vertical or horizontal line, at least one of the products $(x_i-\bar x)(y_i-\bar y)$ is nonzero. Consequently,

When the relationship between $x$ and $y$ is monotonic, the sum of the $(x_i-\bar x)(y_i-\bar y)$ is nonzero: positive when the relationship is a positive one, negative when the relationship is a negative one.

The least-squares slope, being a positive multiple of this sum, therefore is nonzero. The special cases of points along a horizontal line correspond to zero correlation and points along a vertical line correspond to undefined correlation (and undefined least-squares fit), so they are no exceptions to this general conclusion.

The converse of this implication is logically equivalent to it:

When the least-squares slope is zero, the relationship cannot be monotonic (unless the y-values are constant).

For multiple regression with a fit $\hat y = \hat \beta x + \hat \beta_2 x_2 + \cdots \hat \beta_p x_p,$ the coefficient $\hat \beta$ depends on the other variables included in the regression, as described at https://stats.stackexchange.com/a/46508/919. That is, you regress $y$ and $x$ separately against all the other variables and work with their residuals. This is perhaps the simplest way to understand what $\hat \beta=0$ means:

$\hat \beta=0$ implies that after taking out the effects of all other variables, replacing $x$ and $y$ by their residuals $x^\prime$ and $y^\prime$ respectively, then either $y^\prime$ is constant or there is no monotonic relationship between $x^\prime$ and $y^\prime.$

References

If you didn't know the OLS line passes through the point of averages or that the OLS (univariate) slope is proportional to the paired products of the $x$ and $y$ residuals, then please read the introductory section about correlation and regression in Freedman, Pisani, & Purves Statistics (any edition). Older editions are inexpensive and widely available.

My characterization of multiple regression as a univariate regression of the residuals is a core idea in Mosteller, Frederick, John Tukey. 1977. Data Analysis and Regression: A Second Course in Statistics. 1st edition.