Letting the coordinates of $p$ points be $\beta_i,$ $i=1,\ldots, p,$ the signed distances with noise are $$y_{ij} = \beta_i - \beta_j + \epsilon_{ij}=\mathbf{x}_{ij}\beta + \epsilon_{ij}$$ with iid Normal errors $\epsilon_{ij}$ and model matrix $x_{ij,k} = \delta_{ik}-\delta_{jk}.$

Not all $p$ coefficients are identifiable, however, because the distances don't determine the location. But if we arbitrarily fix one of the coefficients, say $\beta_1=0,$ we can estimate all the other locations relative to this one.

This is an Ordinary Least Squares (OLS) problem and so can be solved with the usual OLS machinery.

To illustrate, I generated four random points at locations

1.9 11.6 5.6 9.3

The model matrix $X = (x_{ij, k})$ (with its first column, for $\beta_1,$ omitted) is

Point

Interval 2 3 4

1-2 1 . .

1-3 . 1 .

1-4 . . 1

2-3 -1 1 .

2-4 -1 . 1

3-4 . -1 1

For instance, the first row in this matrix says the distance between points 1 and 2 equals $(1,0,0) (\beta_2,\beta_3,\beta_4)^\prime = \beta_2 = \beta_2-\beta_1$ (because, implicitly, $\beta_1=0$). The last row says the distance between points 3 and 4 is $-\beta_3 + \beta_4.$

The least squares estimates, compared to the locations, are good:

2 3 4

True location 9.8 3.8 7.5

Estimate 9.8 3.1 7.8

(Notice that "true location" is relative to the first point at 1.9.)

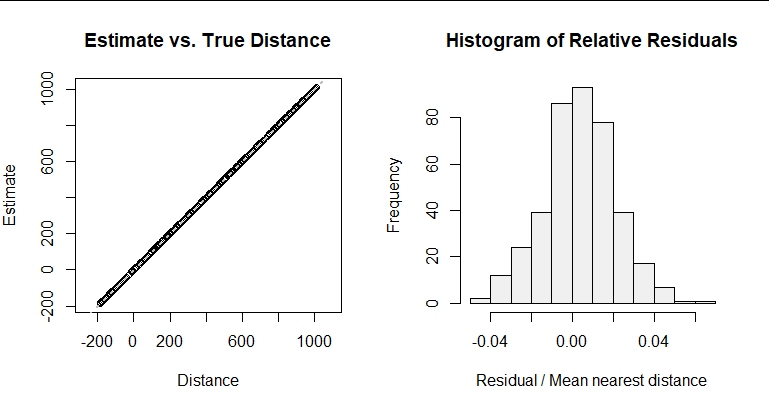

As another illustration, I created 400 random points (at typical inter-point distances of $3$) and measured their $400(399)/2=159\,600$ distances with Gaussian noise of unit standard deviation (which is a fairly large fraction of these distances, making this a stringent test). Rather than print out the results, it's better to graph the $399$ coefficient estimates!

You can see it works very well. The reason is that we have $399$ measurements associated with each point, so the imprecision in each estimate should be about $1/\sqrt{399}\approx 0.05,$ or about $1.7\%$ of the average nearest-neighbor distance. The imprecision is about twice that because these measurements are not independent.

The software fit this model (of $159\,600$ observations and $399$ variables) in a couple of seconds. I used a sparse matrix for $X$ to save RAM.

This is the complete R code for generating the examples and figures. (Change n <- 4 to n <- 400 for the figures.) The estimates are stored in the vector b.

noisy_dist = function(x, sigma=1){

out <- as.matrix(dist(x))

eps <- matrix(0, nrow(out), ncol(out))

i <- lower.tri(eps)

eps[i] <- rnorm(sum(i), 0, sigma)

(out + eps + t(eps)) * outer(x, x, function(i,j) sign(i-j)) # Signed distance

}

#

# Create a noisy distance matrix.

#

set.seed(17)

n <- 4

x <- runif(n, 0, 3*n)

names(x) <- seq_along(x)

if (length(x) <= 10) print(x, digits=2)

D = noisy_dist(x)

if (length(x) <= 10) print(D, digits=2)

#

# Create the model matrix associated with `D`.

#

library(Matrix)

X <- (function(ij) {

f <- function(u)

sparseMatrix(i=seq_len(ncol(ij)), j=ij[u,], x=(-1)^u, dims=c(ncol(ij), max(ij)))

X <- f(1) + f(2)

dimnames(X) <- list(Interval=paste(ij[1,], ij[2,], sep="-"), Point=seq_len(max(ij)))

X

})(combn(seq_len(nrow(D)), 2))

if (length(x) <= 10) print(X[, -1])

#

# Estimate the coefficients.

#

library(MatrixModels)

b <- MatrixModels:::lm.fit.sparse(X[, -1], D[lower.tri(D)])

if (length(b) < 10) round(rbind(`True location`=x[-1] - x[1], Estimate=b), 1)

#

# Display some diagnostic plots.

#

par(mfrow=c(1,2))

plot(x[-1] - x[1], b, asp=1,

xlab="Distance", ylab="Estimate",

main="Estimate vs. True Distance")

abline(c(0,1), lty=3, lwd=2, col="Gray")

sigma <- diff(range(x)) / (length(x) - 1)

hist((b - (x[-1] - x[1])) / sigma, col="#f0f0f0",

main="Histogram of Relative Residuals",

xlab="Residual / Mean nearest distance")

par(mfrow=c(1,1))

lmfunction should fit this beautifully (especially if you fix, say, $\beta_1=0$ to eliminate the inherent non-identifiability). Is your problem perhaps that $p$ is huge? Something else? $\endgroup$Dfrom my code. I'm having trouble discerning what I should be using as the model matrix $x_{ij,k}$ however; I don't follow what $\delta_{ik}$ and $\delta_{jk}$ are intended to be. Would you mind clarifying? $\endgroup$XinRin many ways, such asp <- nrow(D); X <- do.call(rbind, lapply((p-1):1, function(i) cbind(matrix(0, i, p-1-i), -1, diag(1,i,i)))). Then you're all set:lm.fit(X[, -1], D[lower.tri(D)])does the work and the estimates will be its coefficients. For large $p$ you will want to use a sparse array representation of $X,$ because $X$ has $p^2(p-1)/2$ entries but only $p(p-1)$ of them are nonzero. $\endgroup$