I am new to time-series analysis.

I am struggling to interpret the result I got from auto.arima().

I've read the highly-recommended blog https://robjhyndman.com/hyndsight/arimax/. I also read a similar question on ARIMAX vs. Regression With ARIMA Errors but I still got a few more questions.

My code (I was using auto.arima() to analyze daily ridership data in Boston and I did not do any data manipulation beforehand, like taking log or standard scaling on variables) :

weather_indicators = df_2019[['Boston Temperature_mean','Boston Precipitation Total','Boston Evapotranspiration','Boston Sunshine Duration','Boston Relative Humidity_mean']]

model2 = pm.auto_arima(df_2019['Total_Daily'], suppress_warnings=True,exogenous = weather_indicators, seasonal=True, m=7)

I used python here but my understanding is that the pmdarima should be very similar to auto.arima() in R.

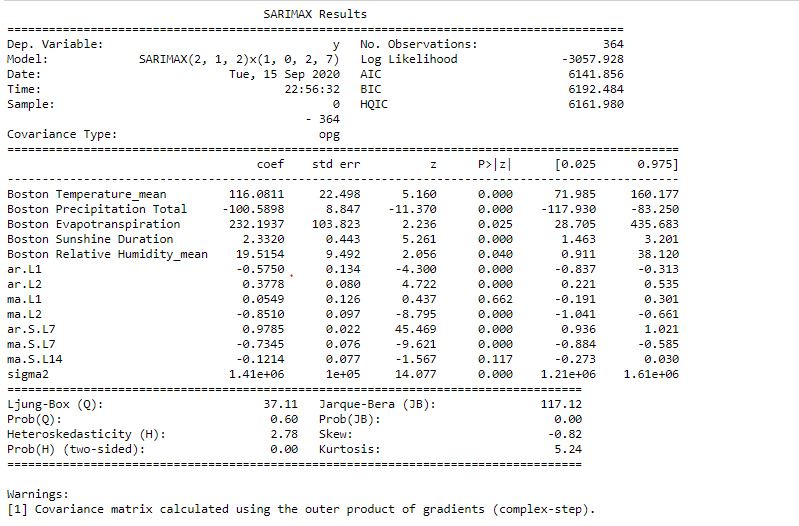

And I got a result looks like this:

The above result is pretty rough but still I would like to know:

1. Interpretation on coefficients

The coefficients for the exogenous variables (especially the first 3 weather variables) are much larger than coefficients for AR and MA. Does that mean the weather is much more statistically significant to the daily ridership number than the time-series factors are? or is it because the auto_arima() is a Regression with ARMA errors, which renders the coefficient for exogenous variables always being much larger than those for AR,MA?

2. ARIMAX vs multiple linear regression

My focus was on studying the effect of the exogenous variables. If time-series factor (coefficients for AR and MA) are not that statistically significant(very low in this case), maybe a multiple linear regression (between daily ridership and different weather variables) would be more appropriate? Or this SARIMAX result is good enough?

Many thanks.