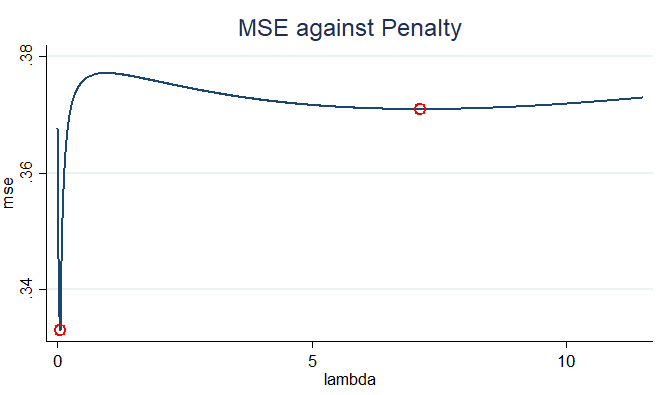

The figure below shows the Test-MSE against $\lambda $, the penalty term. There are two minima, one very close to 0 and the other at around 7.

These are made-up data I wanted to use in an introductory class about the Ridge regression. I did not expect to find two minima. My questions:

- Do multiple minima often arise in practice?

- Is there a standard way to discard one of the minima? (Stata, for example, only reports the larger of the two minima.)

- There seems to be a theoretical result that states that the ridge loss function is strictly convex (on page 17, https://arxiv.org/pdf/1509.09169;Lecture refers to a theorem by Fletcher (2008) and states that the ridge estimator is a global minimum). What assumptions are violated in this example so that the theorem does not apply?

Related question: Can cross validation MSE have multiple minima as function of lambda?

Below the data and Matlab code. Note: this is not meant to be good programming. The students have no experience with programming.

% Generate data

X = [3, 3

1.1 .9

-2.1 -1.9

-2 -2];

y = [1 1 -1 -1]';

[n,p] = size(X);

%% Partition data into 4 folds (with four observations, this corresponds to LOO)

K = 4;

cv = cvpartition(numel(y), 'kfold',K);

%% Loop over lambda

j = 1;

for lambda = 0:0.01:12

mse_OLS = zeros(K,1);

for k=1:K

% training/testing indices for this fold

trainIdx = cv.training(k);

testIdx = cv.test(k);

% train Ridge

pseudo = sqrt(lambda) * eye(p);

Zplus = [X(trainIdx,:);pseudo];

yplus = [y(trainIdx);zeros(p,1)];

b_Ridge = Zplus\yplus;

% compute mean squared error

mse_Ridge(k) = mean((y(testIdx) - X(testIdx,:)*b_Ridge).^2);

end

% average RMSE across k-folds

lambda_vector(:,j) = lambda;

b_Ridge_vector(:,j) = ((((X')*X + lambda*eye(p)))^(-1))*(X')*y;

avrg_rmse_Ridge(:,j) = mean(sqrt(mse_Ridge));

j = j+1;

end

[M,I] = min(avrg_rmse_Ridge)

lambda_opt = lambda_vector(I)

end of code