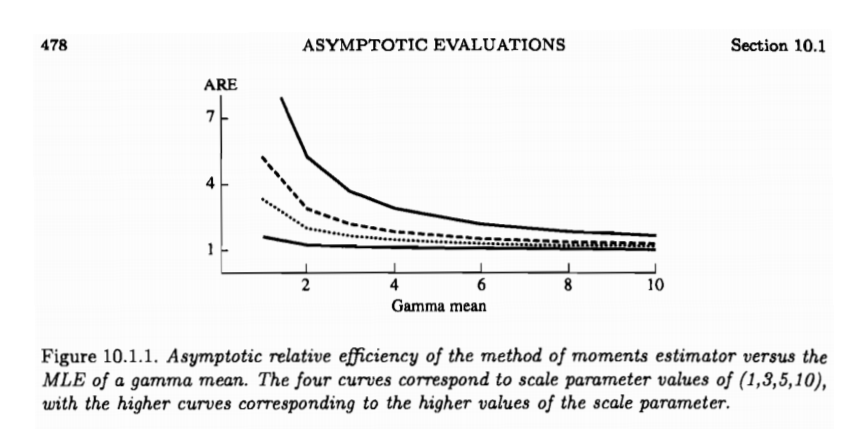

The pictures below are from Statistical Inference by casella berger, page 477-478.

I'm confused on the below example, why does the MLE estimator has a higher asymptotic variance than the sample average for small values of the gamma mean, as shown in the graph figure 10.1.1. The MLE is assumed to by asymptotically efficient, so how could any other estimator triumph in variance? Appreciate any help!