Following problem. I have a daily time series from 2017 to 2021. I want to forecast the time series for each product type and different categories. I have high autocorrelation for nearly 365 lags. Any ideas for forecasting methods? Machine learning seems to be right. But as the only input is past data (no exogenous variables) Support Vector regression does not seem to be optimal.

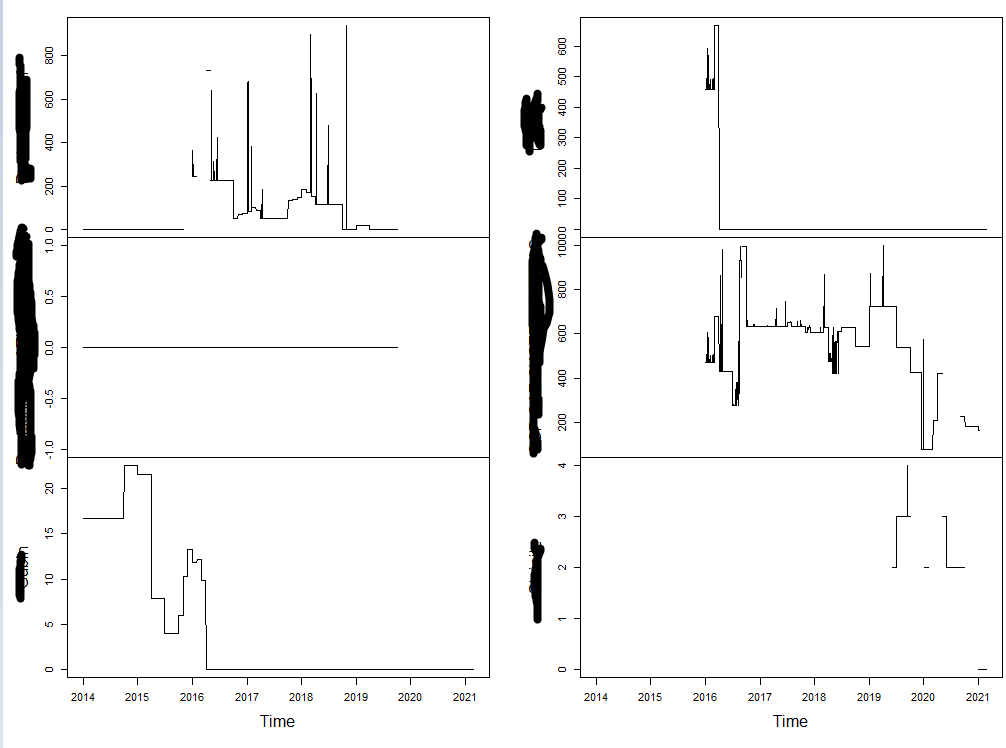

Here some examples Anyone any ideas where to look for forecasting models for such type of data?

Many thanks in advance