I was wondering if there is a package I can use to convert my 22 annual observations to quarterly series?

Will there be any harm in doing so? Will I lose any important data specific information? I want to run VARs in levels using TY method.

I was wondering if there is a package I can use to convert my 22 annual observations to quarterly series?

Will there be any harm in doing so? Will I lose any important data specific information? I want to run VARs in levels using TY method.

Yes, Eviews does that. There are various methods, such as quadratic match method, constant-match average, etc. I am not sure whether it is available in other packages.

Details here.

I don't think this is conceptually possible. I don't know how Eviews can claim to do this (@user1493368's answer). It sounds incredibly dangerous.

Apart from anything else, if you have 22 observations, that is all you have - you cannot somehow pretend you have 88 and then use them in a model as though you had four times as many data points as you do.

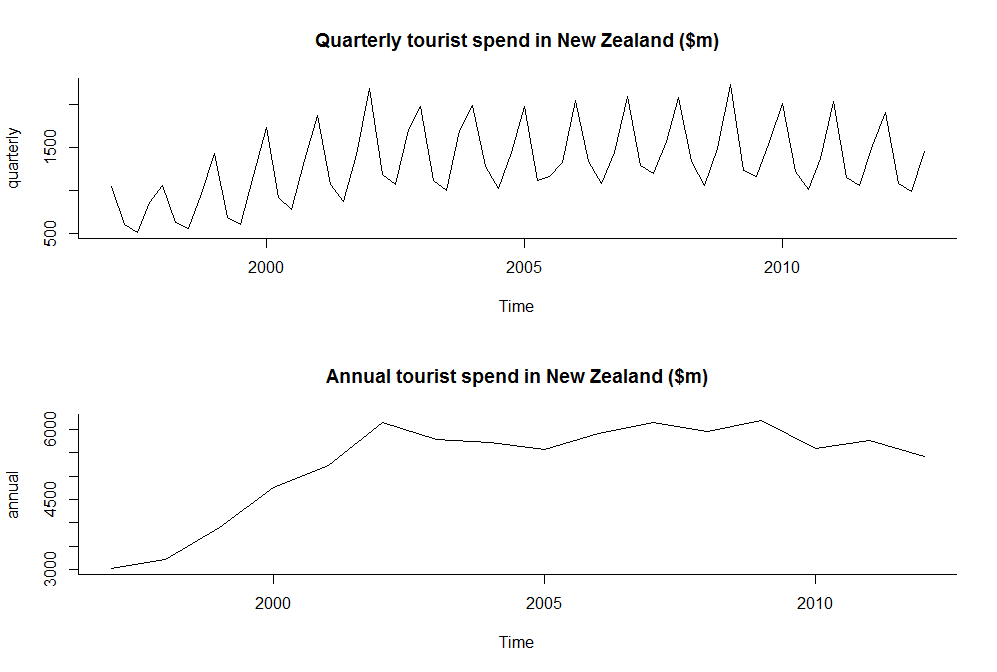

Putting aside that, consider the two series below, which are drawn from real life data. Once you have aggregated up from the quarterly to the annual series, there is simply no way you can go back to the quarterly data, unless you fabricate a) the seasonality and b) the inter-quarter randomness. Of course, you could make some "assumptions" about those two things, but you shouldn't fool yourself that you're doing anything other than arbitrarily making up data.

There are a few methods which can disaggregate time-series but besides the original annual series you need to have a quarterly/monthly indicator series from which the seasonal cycle will be inferred.

These benchmarking and extrapolation methods try to conserve as much as possible from the quarter-to-quarter changes in new series with simultaneously having a binding constraint that the sum of four quarters is same as one value in annual series.

arg min {x} t(x)Ax such that Ra=c, where x is error between bench-marked series a and original higher frequency series b. Vector c contains annual values and R is a matrix of constraints.