I am afraid I am asking a stupid question... but...

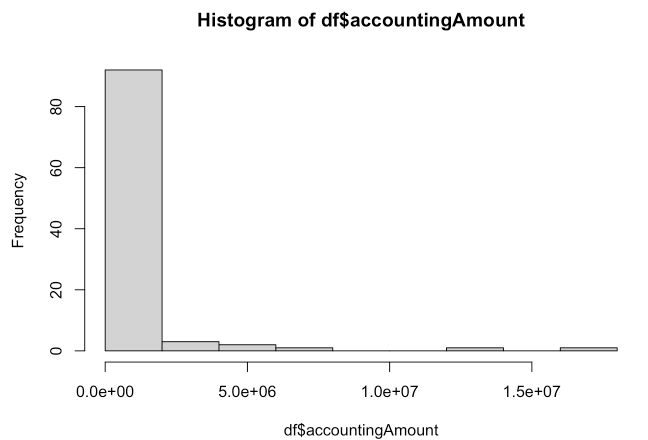

I would like to study the spending (my outcome variable) of a company by department, number of staff, activity, etc. I have collected my data and when I plot the spending, it looks very skewed:

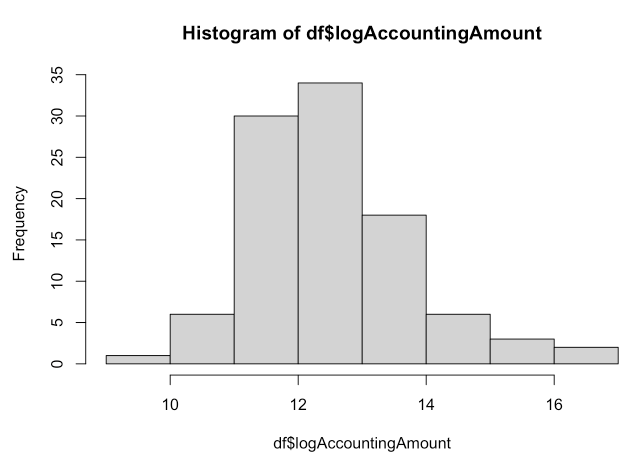

So, I thought it was a good candidate for log-transformation:

which looks more normal.

Then, I ran a linear regression:

lm(log(accountingAmount) ~ Pred1 + Pred2 + Pred3, data=df)

I was thinking of running a GLM Poisson regression but my outcome is not really count (well... I guess it could be considered as count since it is dollars) and its variance is far from being equal to the mean, which does not meet the criteria for Poisson distribution.

I have read different posts (log-linear vs Poisson, Is log-linear a GLM or Poisson regression vs log-linear model), but I could not really find my answer.

Questions

So, is my first approach (using lm(log(accountingAmount) ~ Pred1 + Pred2 + Pred3, data=df)) a good approach? Basically, it is the "standard way" to do log-linear regression?

Is that correct that GLM Poisson regression is not possible in this case (because of very high variance compared to the mean) ?