I would like to use normal copulas to set the dependence of N random variables. That is, I want the correlation $\rho$ to be equal between all variables. I am doing this with the copula package in R. This seems straightforward enough when $\rho$ is positive or when N = 1, however I get odd results when $\rho$ is negative and N > 1:

library(psych)

library(copula)

N = 6 #The number of random variables or dimensions

m = ((N-1)*N)/2 #Number of correlated pairs

correlations = rep(-.95, m) #Set all correlations to be the same value, in this case -0.95

listExp = list(rate = 2)

lists = list(listExp, listExp, listExp, listExp, listExp, listExp) #A list of exponential distributions that is N long

mv.NE = mvdc(normalCopula(correlations, dim = N, dispstr = "un"), rep("exp",N),lists) #create multivariate distribution

x.samp = rMvdc(1000, mv.NE) #sample from multivariate distribution

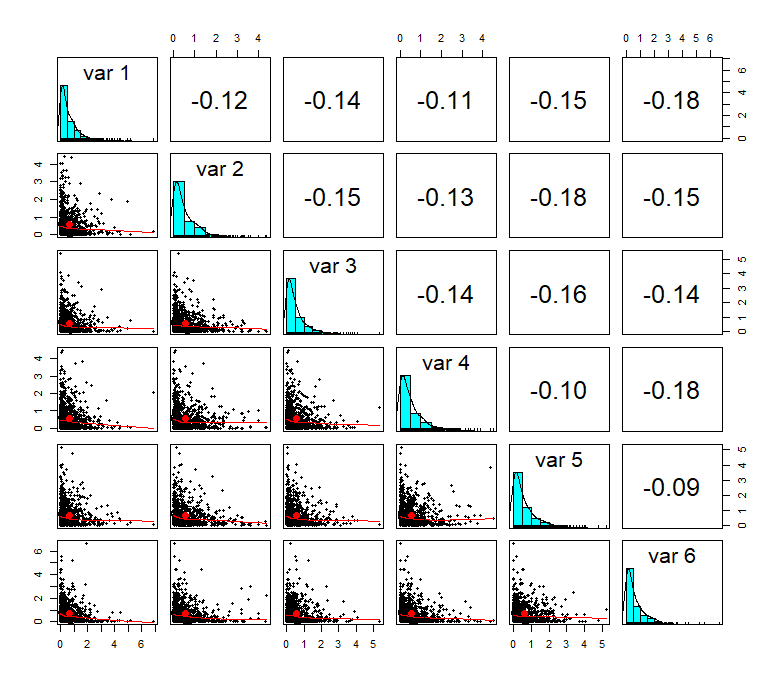

pairs.panels(x.samp) #plot results

As you can see, the measured spearman's correlations are well below the set $\rho$ of 0.95. Does this arise from an error in this script, or is this a fundamental limitation of normal copulas? If its the latter, is there a different method I could use instead?