I am estimating a dynamic factor model which allows the errors to follow an AR(1) process. Thus, an approximate dynamic factor model. So for residual diagnostics I plotted the correlogram of residuals. My question is how to detect an AR(1) process of errors through the correlogram of residuals?

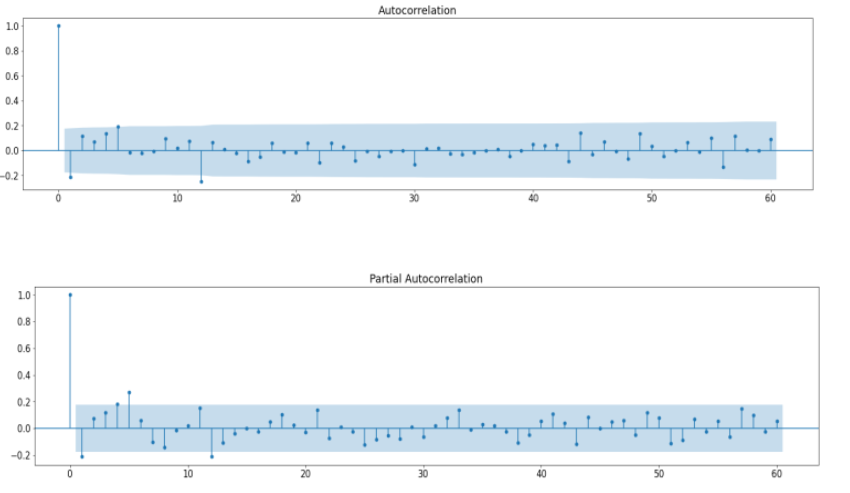

Given below are the ACF and PACF plots I obtained:

$\begingroup$

$\endgroup$

2

-

1$\begingroup$ Determining the lag order of AR(p) by ACF and PACF is a well known and widely discussed exercise with ample textbook coverage and dozens if not hundreds of question on Cross Validated. Is your case somehow special, making these considerations irrelevant? $\endgroup$– Richard HardyCommented Jan 17, 2022 at 13:40

-

$\begingroup$ @RichardHardy I want to know whether the above plots of residuals show an AR(1) process in the context of estimation of approximate dynamic factor models. Is using ACF and PACF plots to check whether residuals follow and AR(1) process a valid methodology? $\endgroup$– Geek_TechCommented Jan 17, 2022 at 13:43

Add a comment

|

1 Answer

$\begingroup$

$\endgroup$

$\endgroup$

8

Is using ACF and PACF plots to check whether residuals follow and AR(1) process a valid methodology?

I suppose it is valid unless there is something special about this model which I do not know. The plots suggests AR(0), AR(1) or AR(5) depending on how sensitive to marginally significant ACs and PACs you want to be. (An AR(12) could also be considered but I think it would be an overkill unless you restricted most of the intermediate lags to zero.)

Note that even the largest ACs/PACs are small in magnitude. If you append your model to adjust for them, you risk introducing more estimation variance than the reduction in the squared bias. So in terms of mean squared error you might be better off leaving your model as is.

answered Jan 17, 2022 at 14:17

-

$\begingroup$ thank you for the explanation Professor. So according to your opinion, is it better to leave the model as it is? Also, you have mentioned "depending on how sensitive to marginally significant ACs and PACs you want to be". ..In order to justify my model is adequate with residuals following an AR(1) process, how should I address the above-mentioned statement? $\endgroup$ Commented Jan 17, 2022 at 14:27

-

1$\begingroup$ @Geek_Tech, it is a subtle matter. We are looking for a good balance between underfitting (leaving genuine patterns of a population unaccounted for in our model) and overfitting (accounting for sample-specific noise variation that is not to be found in the population). Yes, sound inference requires assumptions to be met, but an overfitted model represents noise in addition to the genuine patterns even though the model appears adequate when looking at its residuals. A middle ground is to account for the large (in the subject-matter sense) patterns but leave the small ones unaccounted for. $\endgroup$ Commented Jan 17, 2022 at 19:20

-

1$\begingroup$ @Geek_Tech, I guess I do not have a satisfactory answer. I would keep the model as is for practical use, but that would also entail risking that some picky reviewers would criticize the reliability of the results based on the residual diagnostics. $\endgroup$ Commented Jan 17, 2022 at 19:22

-

1$\begingroup$ @Geek_Tech, what is DB statistic? Durbin-Watson (DW)? DW assesses first-order autocorrelation (AC1), but that is allowed in your model, so we do not care whether AC1 is zero or not. What you need is ACs beyond the first order to see if they are different from zero. That could be tested using Breusch-Godfrey or perhaps Ljung-Box. But a formal test will not tell you more than we already see from the graphs... $\endgroup$ Commented Jan 17, 2022 at 19:44

-

1$\begingroup$ @Geek_Tech, you are welcome! $\endgroup$ Commented Jan 18, 2022 at 6:37