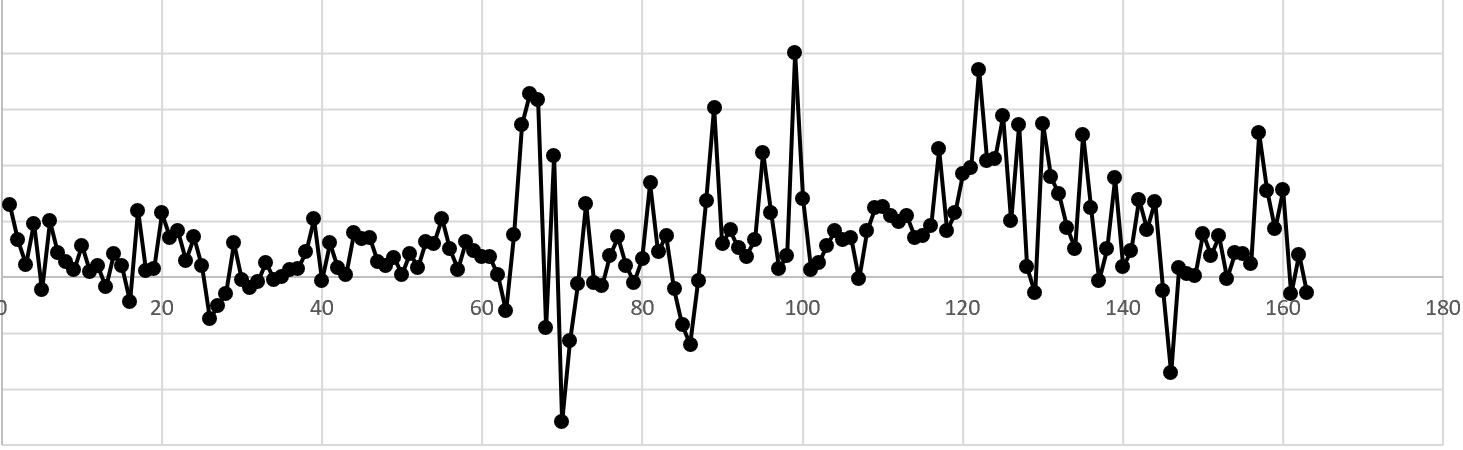

Would this data set be considered stationary or are there too many anomalies around 60-120. If no, would I ignore the anomalies or would I attempt differencing to turn it stationary?

Would this data set be considered stationary or are there too many anomalies around 60-120. If no, would I ignore the anomalies or would I attempt differencing to turn it stationary?

This time series does not appear stationary, as its variance changes over time. The fluctuations between periods 0 and 60 are relatively small, while the fluctuations between periods 60 and 100 (or perhaps the whole way until period 160) are relatively large, perhaps 3 times as large as the former ones. This is known as (conditional) heteroskedasticity and is a violation of stationarity.

Note that differencing will not help. First, that will not remove the heteroskedasticity that you would like to remove to achieve stationarity. Second, the series does not appear to have a unit root, so there is no reason to difference. Differencing a time series that does not have a unit root results in overdifferencing (it introduces a unit-root moving-average component in the process and thus effectively doubles the error variance).

What you could do instead is build a model that allows for time-varying variance or, if variance is just a nuisance feature, ignore variance in the model but use an estimator that is robust to heteroskedasticity. The former approach is a cleaner one, as it offers a more apt description of the process and does not sacrifice precision or power. The latter one may be easier to implement using some standard HAC estimator.