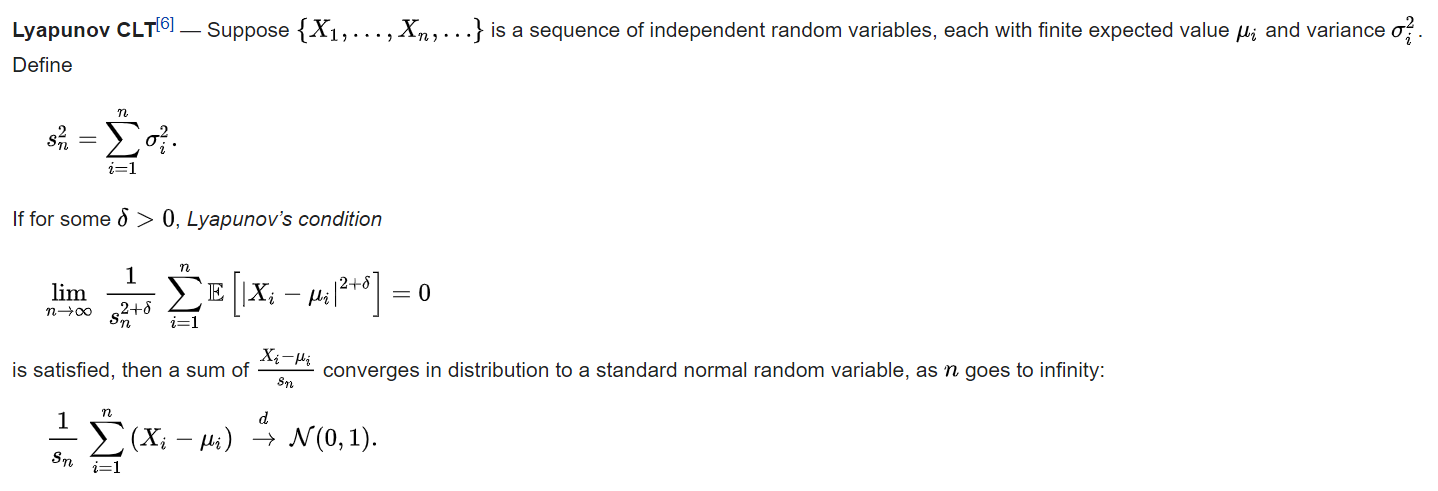

The univariate version of the Lyapunov CLT (a version of the CLT for independent but not necessarily iid random variables) is as follows according to Wikipedia:

Is there a multivariate version of the Lyapunov CLT (ideally one that doesn't require the means of the random variables to all be zero vectors)? I'm having a very hard time finding any information on this, even on Google Scholar.