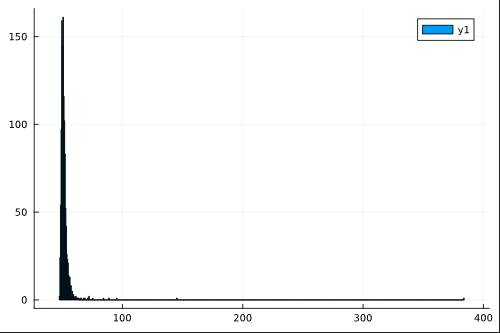

I am running a Monte Carlo simulation that results in an heavy-tailed distribution. The image below shows the distribution of 1,200 runs of the Monte Carlo simulation, where each run consists of integrating over $M$ = 12,000 randomly drawn paths of $ \mathcal{X}_m = \left\{X_{n,m},s_{n,m}\right\}_{n=1}^N$.

The quantity I am simulation is an expectation of a definite sum of exponentials, where I know the sum converges as $N \rightarrow \infty$.

$$\mathbb{E} \left[ S\left(\mathcal{X}\right) \middle| X_1, s_1 \right] = \mathbb{E} \left[\exp\left( X_1\right) + \exp\left(X_1 + X_2\right) + \cdots + \exp\left(X_1 + X_2 + \cdots + X_N\right) \middle| X_1, s_1 \right]. $$

$X_n$ is a Markov-switching Autoregressive process with Gaussian errors:

$$X_n = \alpha_{s_n} + \rho_{s_n} X_{n-1} + \sigma_{s_n} \epsilon_n,$$

where $\epsilon_n \sim N(0,1)$, $s_n \in \{1,2\} \sim \Pi$, and $\Pi$ is a transition matrix.

For a single realization of what is presented in the histogram, I compute $S(\mathcal{X}_m)$ for each of the $M$ simulated paths. And then I simply take an average over the $M$ realizations,

$$\mathbb{E}\left[S\left(\mathcal{X}\right) \middle| X_1, s_1 \right] \approx \frac{\sum_{m=1}^M S(\mathcal{X}_m)}{M}.$$

I believe Monte Carlo should result asymptotically in a normal distribution, but this resembles a log-normal distribution. How would I diagnose this issue? How should I change my simulation strategy?

I've proved the sum converges. The proof boils down to the unconditional mean of $X_n <0$, and sum inside the exponential goes to negative infinity faster than one-half the unconditional variance.

The instability occurs when the sum inside the exponential terms is greater than 0 for a few periods (the process is persistent). Even though it will eventually converge to -$\infty$, and can blow up temporarily.