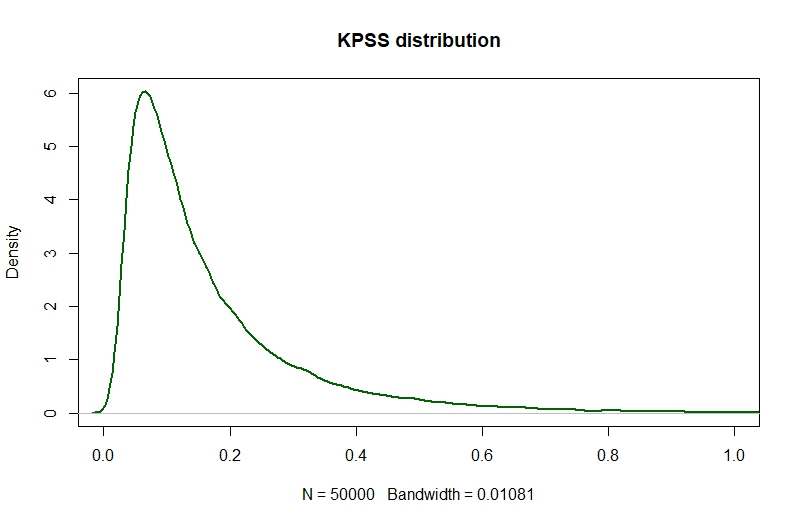

I want to apply a Bonferroni correction on multiple KPSS tests for stationarity. I have $m$ tests, and so I want to see if the p-values are less than $0.01/m$.

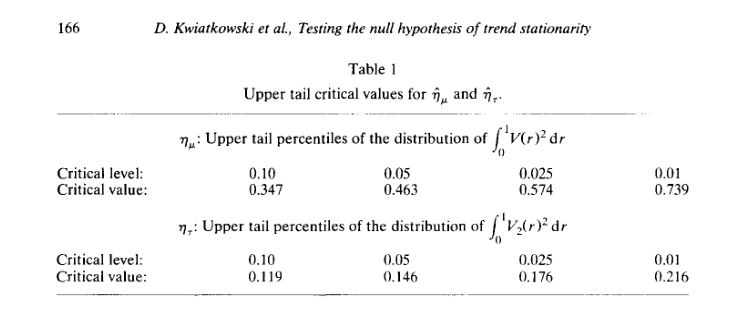

The problem is that the statistical packages (statsmodels.tsa.stattools.kpss in python and kpss.test in R) report p=0.01 if the test statistic is above the critical threshold. They don't report p-values below 0.01. The thresholds are given in the original paper: Kwiatkowski, D.; Phillips, P. C. B.; Schmidt, P.; Shin, Y. (1992). "Testing the null hypothesis of stationarity against the alternative of a unit root".

The test distribution is non-standard. Does anyone have an idea how to do this? I imagine I can follow the original paper and compute new critical values for my adjusted significance, but that would be a lot of work. Anyone encountered this problem before? Or know a quick way to adjust the p-values?

The critical values for $\alpha=0.001$ is 1.16786, according to Nabeya, Seiji, and Katsuto Tanaka. "Asymptotic theory of a test for the constancy of regression coefficients against the random walk alternative." The Annals of Statistics (1988): 218-235. This was also cited in the Kwiatkowski et al paper.