I am struggling with a time series dataset comprising 12 features, including quantity sold and weather data, totaling approximately 1800 values, where data is recorded on a daily basis. My goal has been to forecast future values, quantity sold, for the next 7 days for a specific item. Despite exploring various avenues, I have not yet identified an optimal model for accurate predictions. Here's a summary of my attempts:

ARIMA Model: I began with the ARIMA model, experimenting with different combinations of parameters (p, d, and q) during training. However, my R-squared values for test data never exceeded 0.45. Even visual inspection revealed that the model did not fit the test data well.

model = SARIMAX(df_train[item],order=(5,1,0),seasonal_order=(1,1,1,60), enforce_stationarity=False, enforce_invertibility=False)

ADF Statistic: -3.7660612647232545

p-value: 0.0032742778913118914

Lags Used: 23

Number of Observations Used: 1800

Critical Values:

1%: -3.4339881389288407

5%: -2.863147035877915

10%: -2.567625533641975

Reject the null hypothesis (H0). The data is stationary.

Here are some plot:

- Machine Learning Models: I also delved into machine learning techniques, including XGBoost, Random Forest, and others. Despite my efforts, I couldn't achieve R-squared values higher than 60%.

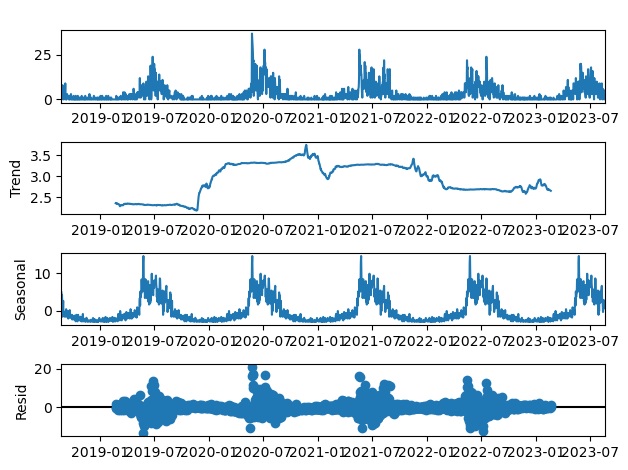

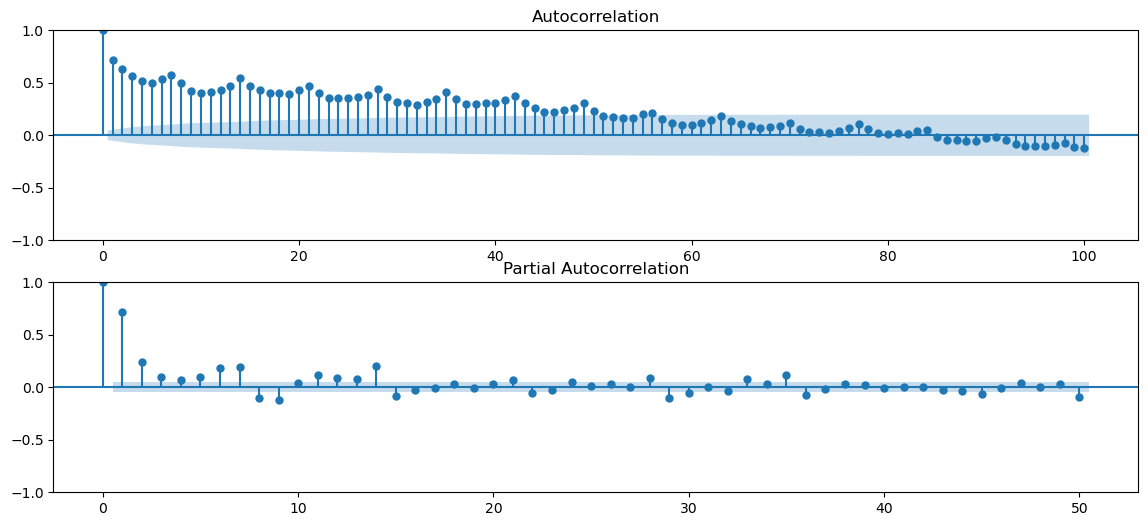

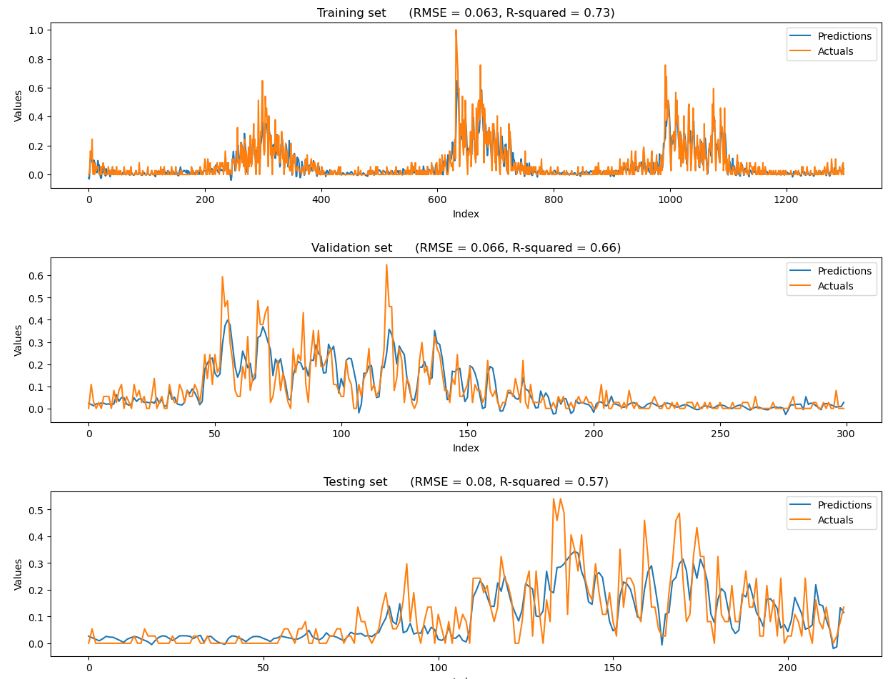

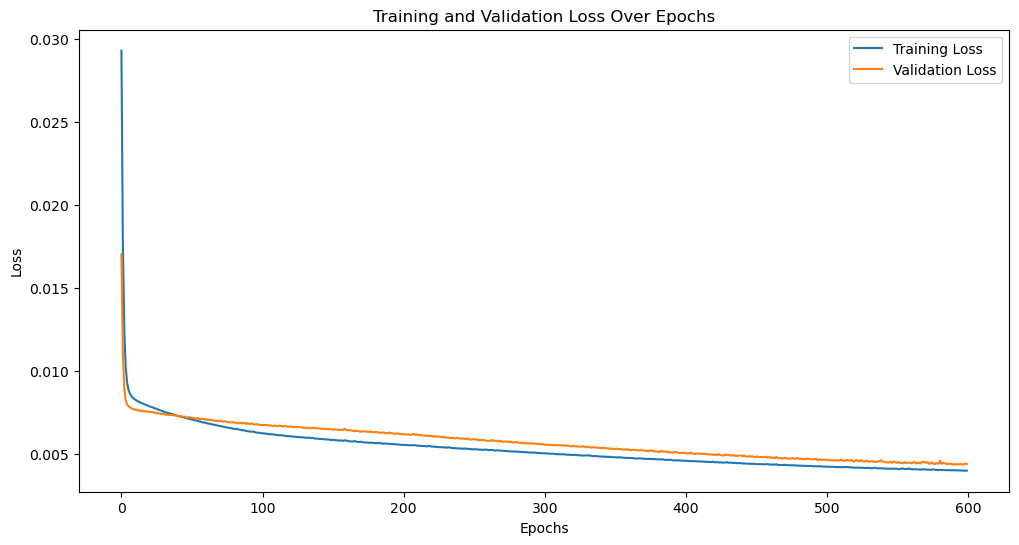

- LSTM (Long Short-Term Memory): In addition, I explored the LSTM model, a type of recurrent neural network commonly used for time series forecasting. Unfortunately, this approach did not yield satisfactory results either. I will provide some plots related to the LSTM model, which will offer deeper insights into the dataset. These visualizations will aid in understanding the structure of the target variable and other essential properties.

I've implemented the model with a learning rate of 1E-5. I experimented with higher rates, but this particular value has yielded the most promising results thus far. Additionally, I fine-tuned the hyperparameters using GridSearch and KerasRegressor to optimize the model's performance.

model = Sequential()

model.add(InputLayer((7, temp_df.shape[1])))

model.add(LSTM(128))

model.add(Dense(8, 'relu'))

model.add(Dense(1, 'linear'))

model.compile(loss=MeanSquaredError(), optimizer=Adam(learning_rate=1E-5), metrics=[RootMeanSquaredError()])

early_stopping = EarlyStopping(monitor='val_loss', patience=10, restore_best_weights=True)

model.fit(X2_train, y2_train, epochs=5000, batch_size=32,

validation_data=(X2_val, y2_val), callbacks=[early_stopping], verbose=1)

Please note that I applied normalized data, MinMaxScaler(), and incorporated time-dependent features extracted from the date in all the models. I extensively tested various combinations, yet none of them yielded superior results. Despite these challenges, I am continuing my search for a suitable model that can effectively predict future values in this complex dataset.

I believe there are crucial aspects I might be overlooking while trying to solve this model. I would be grateful if you could point out specific areas or provide insights that could help me address these challenges effectively. Your guidance would be greatly appreciated.

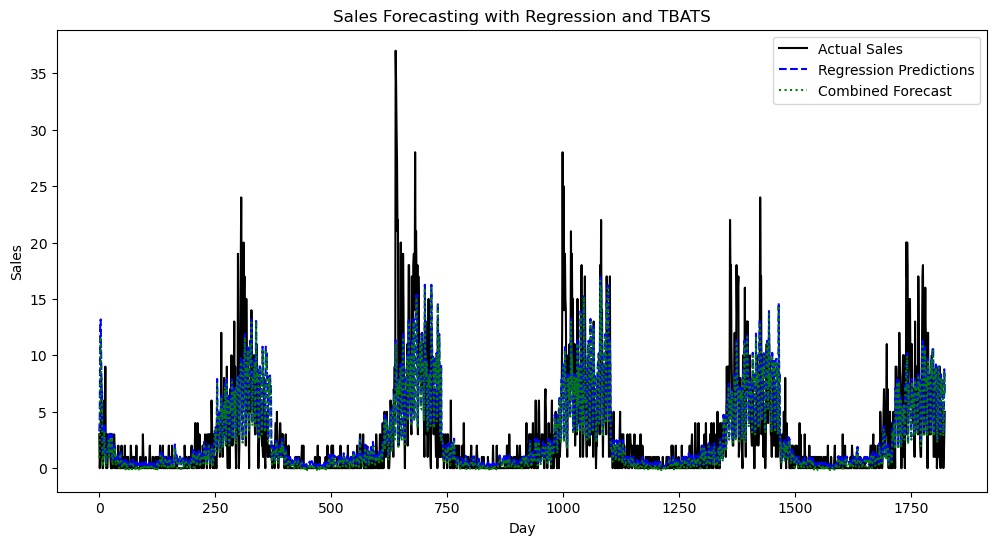

- EDITED version with poisson regressor. I see there is some improvement compare to previous model using LinearRegressor.

poisson_model = sm.GLM(y, X, family=sm.families.Poisson())

tbats_model = TBATS(seasonal_periods=(7, 365.25))

r2 Score (Regression): 0.5563435836305534

RMSE (Regression): 2.9807373184768573

r2 Score (Combined Forecast): 0.5547685856536695

RMSE (Combined Forecast): 2.9860234992906065