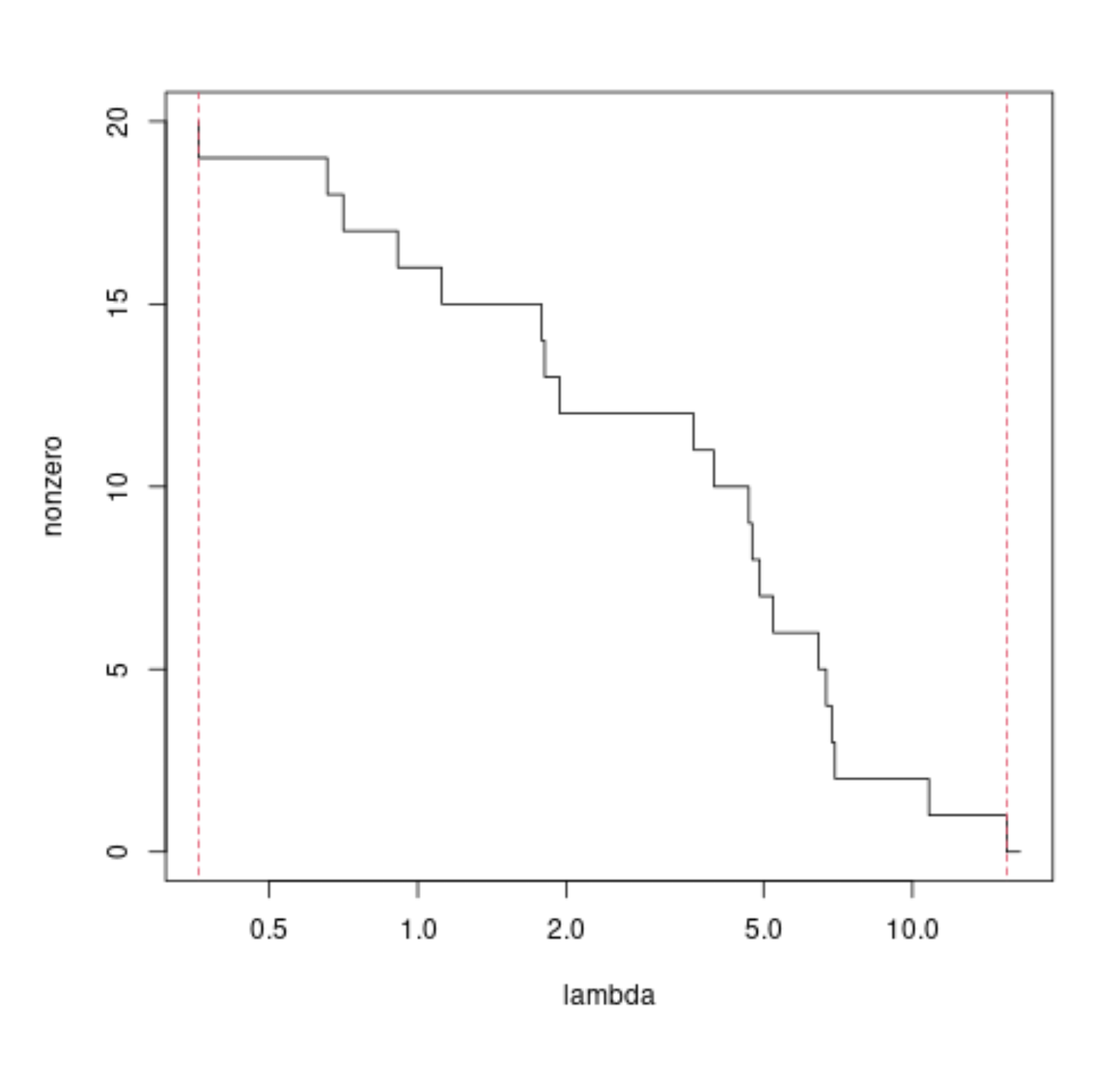

There are simple relationships for the bounds of $\lambda$ where you get all coefficients zero and where you get none of the coefficients zero.

A demonstration of the above formula's with some code

library(lars)

### generate some data

set.seed(1)

n = 50

m = 20

X = matrix(rnorm(m*n),n)

y = rnorm(n)

### perform lasso

mod = lars(X,y, intercept = 0, normalize = 0)

nonzero = rowSums(mod$beta^2 > 0)

lambda = mod$lambda

lambda = c(lambda[1]+1,lambda) # add one additional point

### plot the number of nonzero estimated coefficients

### as function of lambda

plot(lambda,nonzero, log ="x", type = "s")

### upper bound above which all coefficients are zero

l_max = max(abs(t(X) %*% y))

lines(l_max*c(1,1), c(-1,m+1), lty = 2, col = 2)

### lower bound below which all coefficients are non-zero

mod = lm(y~0+X)

beta = mod$coefficients

bl = - solve(t(X)%*%X) %*% sign(beta)

bln = bl/sum(bl*sign(beta))

br = beta/bln

d = min(br[br>0])

l_min = sum((X %*% bln)^2)*d

lines(l_min*c(1,1), c(-1,m+1), lty = 2, col = 2)

A simple algorithm to compute the path of solutions to LASSO is least angle regression.

A difficulty to compute directly the value of the penalty $\lambda$ where a particular coefficient becomes non-zero is that it depends on which other coëfficiënts are already non-zero.

This is because of correlations between the coefficients, which makes that the increase of one coefficient can reduce the effect of another. For example one may get even a situation where a coefficient reduces in magnitude as we decrease the penalty (Why under joint least squares direction is it possible for some coefficients to decrease in LARS regression?). Sometimes a coefficient can change from positive to negative (cross zero) as we change the penalty parameter (https://stats.stackexchange.com/a/594633/) and the number of non-zero components as function of the penalty parameter can be a non-monotonic function.

It is easy to compute the points in the paths when either:

We only look at the beginning or the end, as is done in this answer.

When there are no correlations between the regressors, as is done in the answer by EdM.