In Brockwell and Davis' Introduction to Time Series and Forecasting,

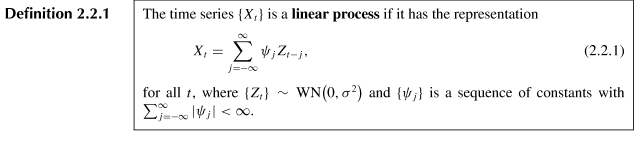

a linear process is defined to be

An ARMA process/model is defined to be

Note that by "stationary", the book means "wide-sense stationary".

An ARMA process can also be written as a form of linear process

- Is it correct that a stochastic process is an ARMA process, if and only if it is a linear process and also wide-sense stationary?

- Despite that the definition of an ARMA process says $X_t$ only depends on past values of $X$ and $Z$, is it correct that an ARMA process may not be causal, because the solution to (3.1.1) is (3.1.3)? Note a causal ARMA process is defined in (3.1.5) here. Do I misunderstand something?

Thanks and regards!