I'm working on a classification problem with ~90k data rows and 12 features. I'm trying to tune the hyperparamters of an XGBoost model to minimize the overfitting. I use ROC_AUC as the metric to evaluate the model performance. With the default XGBoost parameters, the 5-fold CV results show train-auc 0.782 and test-auc 0.739 respectively. This indicates overfitting since train set performs better than the test set.

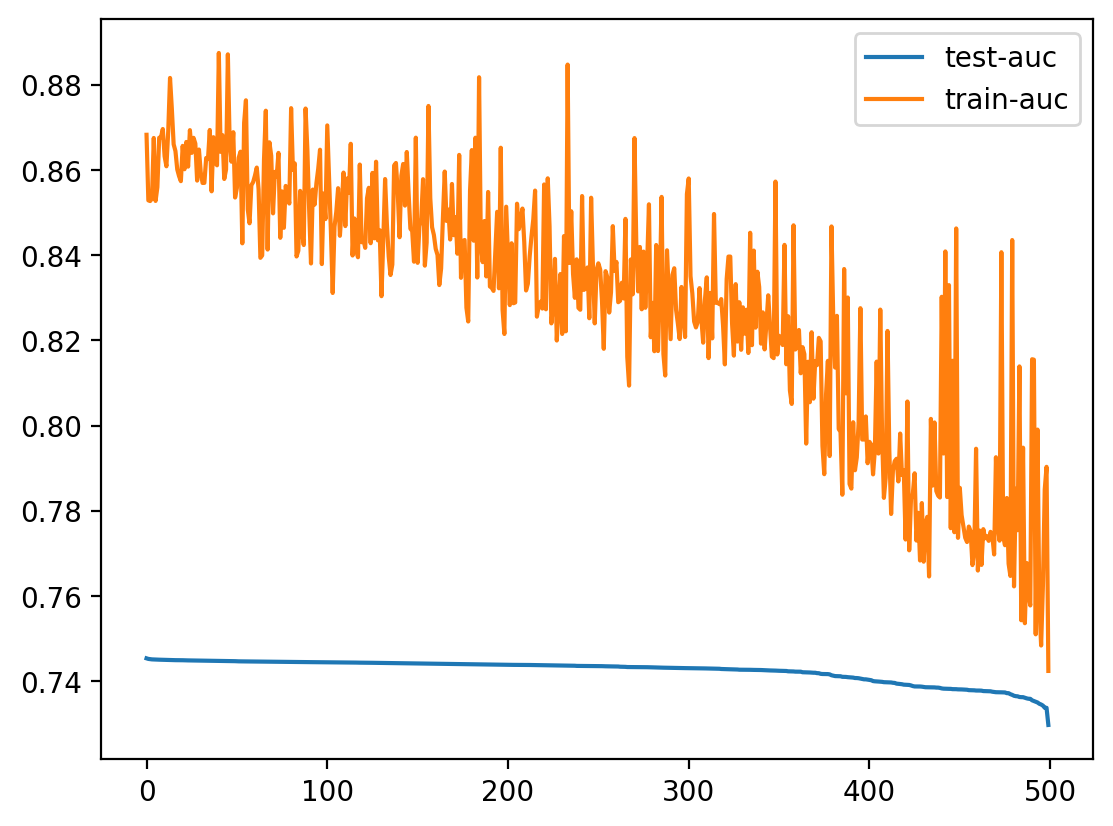

I started tuning the hyperparameters because a), it should be tuned, b) hyperparameters are known to be used to reduced overfitting. However, like many others did, I set the validation-auc as the objective and implemented cross-validation in the objective function. The library used are Optuna and Hyperopt. Interestingly, for both cases, I found the train-test auc gap (indicator of overfitting) widens as the algorithm tries to push the validation-auc towards 0.745. If I plot the train and validation auc in the order of descending validation-auc, the validation-auc decreases from 0.745 to 0.729 while the train-auc drops from 0.868 to 0.742.

I'm quite puzzled by the results. Was I right to set the validation-auc as the objective for Optuna to optimize? Should I have chosen (train-auc - validation-auc) instead, but I haven't found any examples like this online. And should I look at the result and pick the lowest validation-auc and the associated hyperparameter values as the 'best params' since the train-validation metric gap is the lowest?

Please share your thoughts here since as I was typing, I've become unsure about my understanding of overfitting was even correct.

My code:

X, y = df[features], df[target]

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size = 0.2,

random_state = 42, stratify = y)

dtrain = xgb.DMatrix(X_train, label = y_train, enable_categorical = True)

dtest = xgb.DMatrix(X_test, label = y_test, enable_categorical = True)

def objective(trial):

params = {'max_depth': trial.suggest_int('max_depth', 3, 10),

'min_child_weight': trial.suggest_int('min_child_weight', 1, 100),

'gamma': trial.suggest_float('gamma', 0, 2),

'subsample': trial.suggest_float('subsample', 0.5, 1),

'colsample_bytree': trial.suggest_float('colsample_bytree', 0.5, 1),

'reg_alpha': trial.suggest_float('reg_alpha', 1e-8, 10, log = True),

'reg_lambda': trial.suggest_float('reg_lambda', 1e-8, 10, log = True),

'learning_rate': trial.suggest_float('learning_rate', 0.001, 0.3),

'objective': 'binary:logistic'}

cv_results = xgb.cv(

params, dtrain, num_boost_round = 10000, early_stopping_rounds = 50,

metrics = 'auc', nfold = 5, stratified = True, shuffle = False

)

trial.set_user_attr('n_estimators', len(cv_results))

trial.set_user_attr('train-auc', cv_results['train-auc-mean'].iloc[-1])

return cv_results['test-auc-mean'].iloc[-1]

study = optuna.create_study(

direction ='maximize', sampler = optuna.samplers.TPESampler(seed = 42))

study.optimize(objective, n_trials = 500, n_jobs = -1)