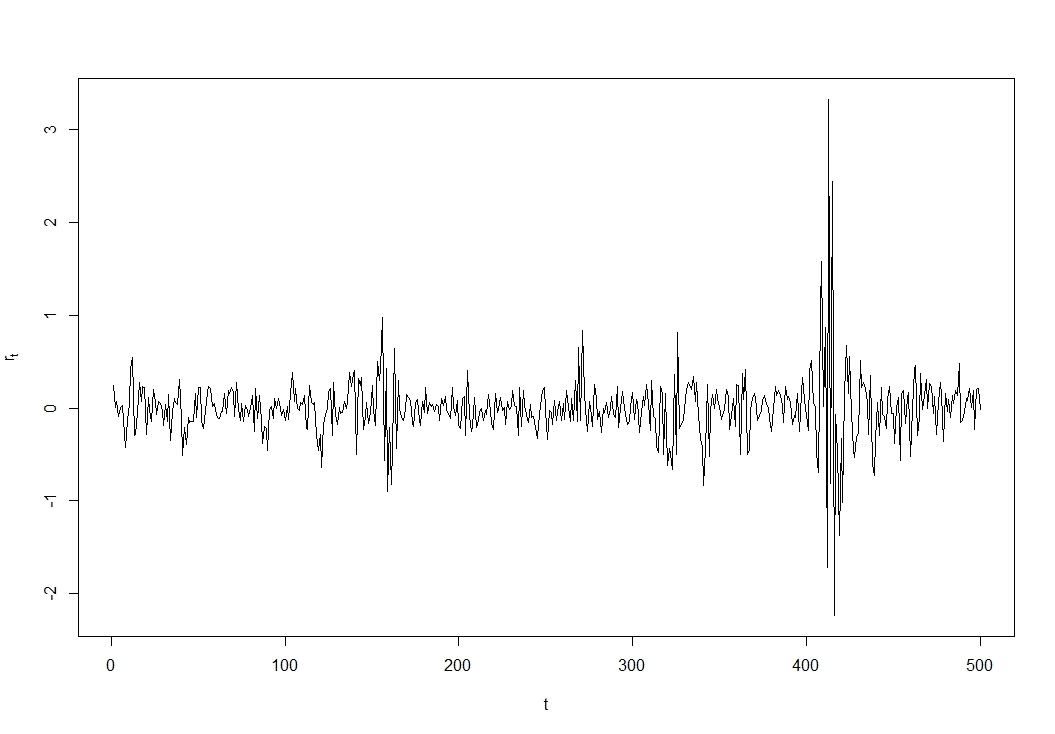

In finance, GARCH (generalized autoregressive conditional heteroskedasticity) effects are widely cited here: stock returns $r_t:=(P_t-P_{t-1})/P_{t-1}$, with $P_t$ the price at time $t$, themselves are uncorrelated with their own past $r_{t-1}$ if stock markets are efficient (else, you could easily and profitably predict where prices are going), but their squares $r_t^2$ and $r_{t-1}^2$ are not: there is time dependence in the variances, which cluster in time, with periods of high variance in volatile times.

Here is an artificial example (yet again, I know, but "real" stock return series may well look similar):

You see the high volatility cluster around in particular $t\approx400$.

Generated using

library(TSA)

garch01.sim <- garch.sim(alpha=c(.01,.55),beta=0.4,n=500)

plot(garch01.sim, type='l', ylab=expression(r[t]),xlab='t')