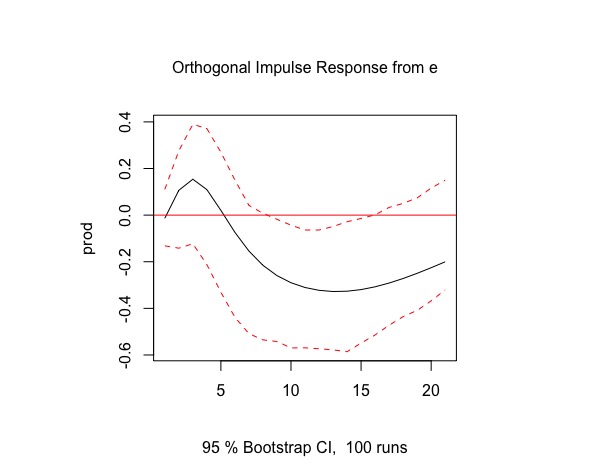

I have a question related to the interpretation of Impulse Response Function (IRF) functions. Assume we do have two time-series that have been both log-transformed and are stationary. When applying a IRF in the vars package, how do we "read" the x and y-axis correctly?

Example:

# Load data and apply VAR

library("vars")

data(Canada)

data <- Canada

data <- data.frame(data[,1:2])

var <- VAR(data, p=3, type = "both")

plot(irf(var, impulse = "e", response = "prod", boot = T, cumulative = FALSE, n.ahead = 20, ci=0.95))

Which interpretation is correct?

- A 1% log-increase of

ecauses a 15% increase ofprodat lag 3? - A 1% increase of

ecauses a 15% log-increase ofprodat lag 3? - Both is wrong, correct is:

Thanks for your help!