I'd like to generate a random square matrix such that the rows are normalized to one and the diagonal elements are the maximum of their column. If there an efficient way to sample from these matrices uniformly?

The motivation is to generate likelihood matrices, with the rows being states of the world and columns being observed signals. Each signal is most likely to occur in its corresponding state, but isn't necessarily the most likely signal in that state.

Edit: The exact distribution doesn't matter, other than it seem natural. I would like to avoid the diagonal also being maximal for the rows though.

Here is my own previous ah-hoc attempt.

gen.likelihood.matrix <- function(T){

# T: Number of states

mat <- matrix(runif(T^2), nrow=T) # Intialize with uniform variates

diag(mat) <- 1 # To guarantee diag is max in column

candidate.mat <- matrix(nrow=T, ncol=T)

# Loop to check for constraint satisfaction

for(k in 1:100){

weights <- runif(T-1)

weights <- weights / sum(weights)

for(i in 1:T){

# Rescale columns

candidate.mat[i,-T] <- mat[i,-T] * weights

# Replace last column with complement to meet row constraint

candidate.mat[i,T] <- 1 - sum(candidate.mat[i,-T])

}

# Does the last column meet the maximality constraint?

if(candidate.mat[T,T] > max(candidate.mat[-T,T])){

# Shuffle to minimize the distortion from last column

reorder <- sample(1:T,T)

return(candidate.mat[reorder,reorder])

}

}

# Recurse to get new initial values if necessary

return(genLikeliMatrix(T))

}

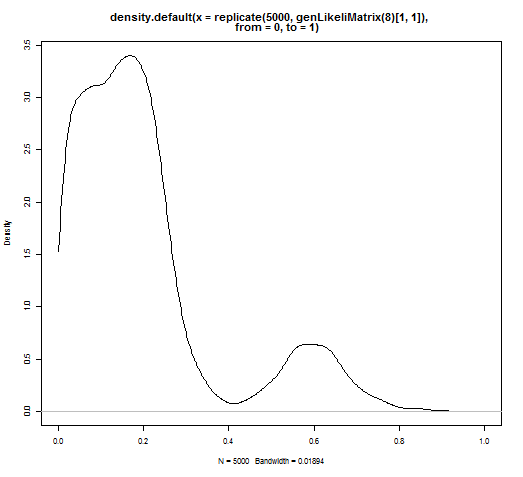

This works in terms of giving me matrices efficiently, but I get a weird bimodal distribution on the diagonal due to how I handle the last column.