In these days I'm working with Breusch-Pagan to test homoscedasticity.

I've tested the prices of two stocks with this method. This is the result:

> mod <- lm(prices[,1] ~ prices[,2])

> bp <- bptest(mod)

> bp

studentized Breusch-Pagan test

data: prices[, 1] ~ prices[, 2]

BP = 0.032, df = 1, p-value = 0.858

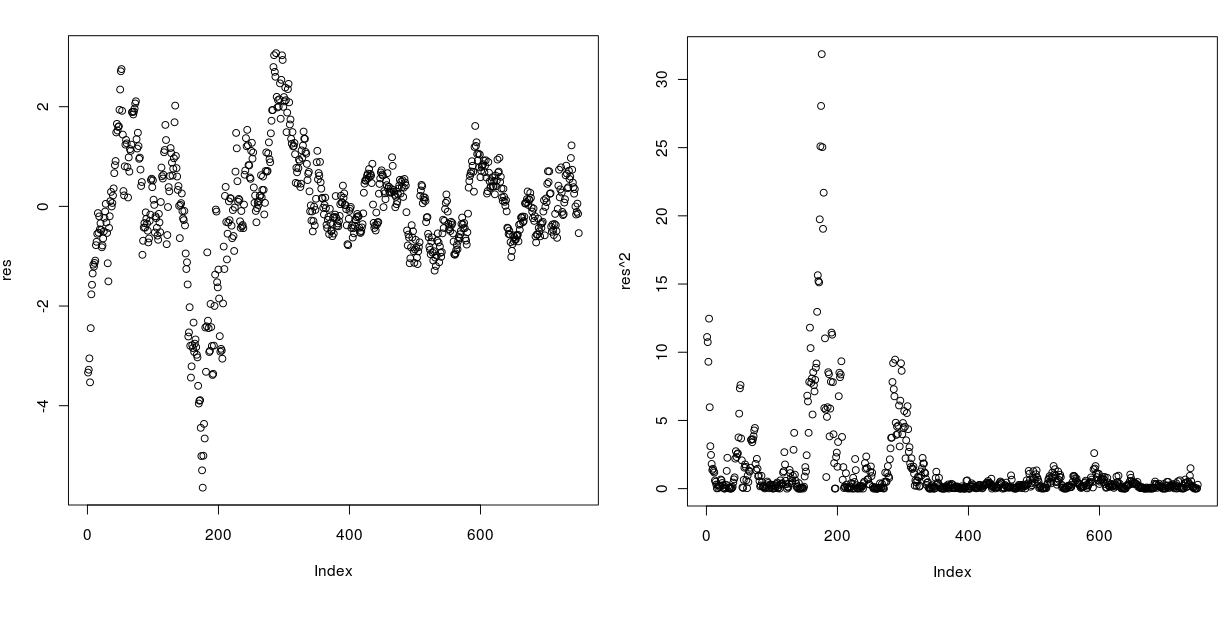

Reading the result the series should be homoscedastic, but if I plot the residuals and the squares residuals it seems totally not! Take a look below:

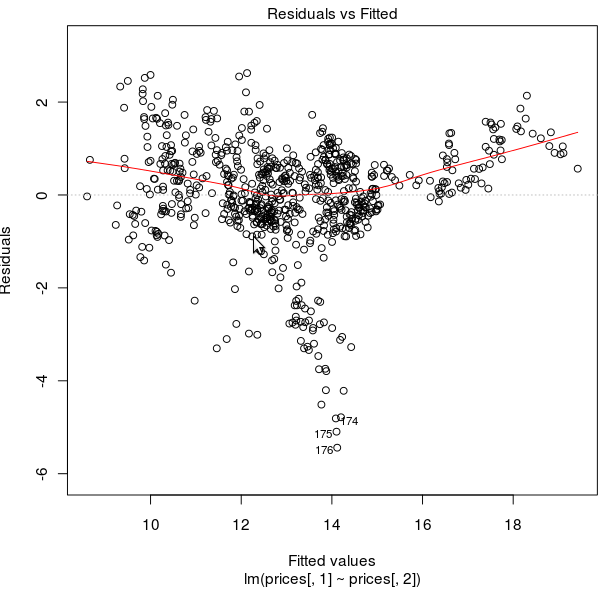

the Residuals Vs FItted below:

How is it possible this series pass the test with a very high p-value?