Take an example of a linear regression,

$Y= \beta X$

where X and Y values are z-score transformed ($\mu$ = 0, $\sigma$ = 1).

In this situation the correlation coefficient $r$ equals $\beta$ because the following equality

$\beta = r \sigma_y/\sigma_x $.

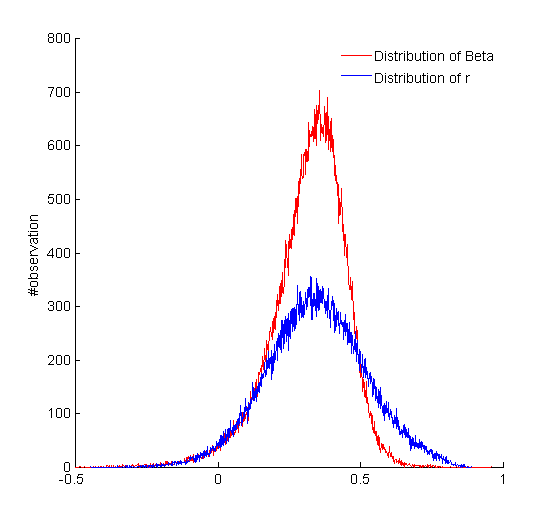

While deriving bootstrap confidence intervals, I was surprised by the observation that beta and r have different bootstrap distributions:

The mean of these two distributions coincides with each other. However the confidence intervals are different, while confidence interval of $r$ includes zero, this was not true for the confidence interval of $\beta$, suggesting a significant contribution. Based on the observation on $\beta$, one might conclude that the regression is significant, whereas $r$ is not different than zero.

It was interesting (well at least for me) to realize that the equality of $\beta$ and $r$ in the equation above, does not imply equality of their distributions. I would be happy to learn more what is really happening here.