All I know is that we assume zero conditional mean (and hence zero mean) and conditional homoscedasticity (and hence homoscedasticity).

When trying to prove that $E[(\hat{\beta_1} - \beta_1)\bar{u}] = 0$, where $\beta_1$ is the slope in the linear regression model, $\hat{\beta_1}$ is its estimate and $\bar{u}$ is the average of the errors in the linear regression model (not the residuals!), I encountered:

$$E[(\hat{\beta_1} - \beta_1)\bar{u}|x]$$

$$\vdots$$

$$ = \frac{1}{n}\sum_{i=1}^{n} \frac{(x_i - \bar{x})}{SST_x} \color{red}{[\sum_{j=1}^{n} E[(u_i)u_j|x]]}$$

$$ = \frac{1}{n}\sum_{i=1}^{n} \frac{(x_i - \bar{x})}{SST_x} \color{red}{\sigma^2}$$

$$\vdots$$

$$ = 0 $$

$$\to E[(\hat{\beta_1} - \beta_1)\bar{u}] = 0$$

QED

What is the justification for that part? I tried:

For $i \ne j$, we have $E[(u_i)u_j|x] = Cov[u_i,u_j|x] + E[(u_i)|x]E[u_j|x] \stackrel{(*)}{=} 0 + (0)(0) = 0$

For $i = j$, we have $E[(u_i)u_j|x] = E[(u_i^2)|x] = Var[u_i|x] = \sigma^2$

Is $(*)$ right?

If so, what is the justification?

If not, how does one show that $E[u_i u_j | x] = 0$?

From Wooldridge:

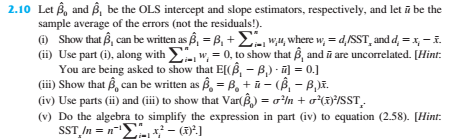

This is from $(ii)$ of this exercise: