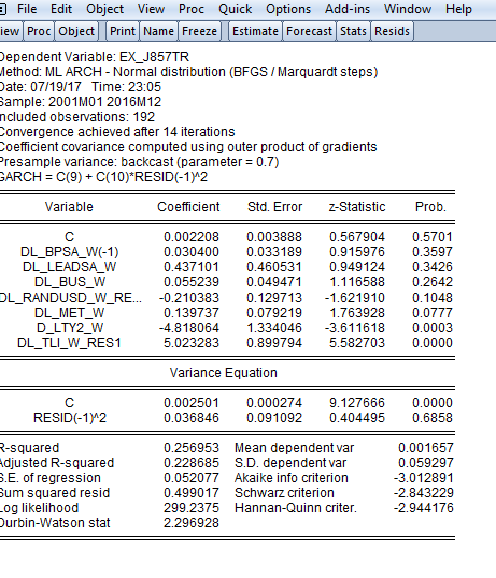

I am trying to estimate a restricted and unrestricted version using the ARCH/GARCH framework. Specifically, I am using a GARCH(1,1) model and am assuming a normal distribution. While I am not really interested in the the conditional variance, I am interested in achieving coefficient efficiency. Two of my variables are orthogonal to all other variables in the model. The resticted version on the model is as follows:

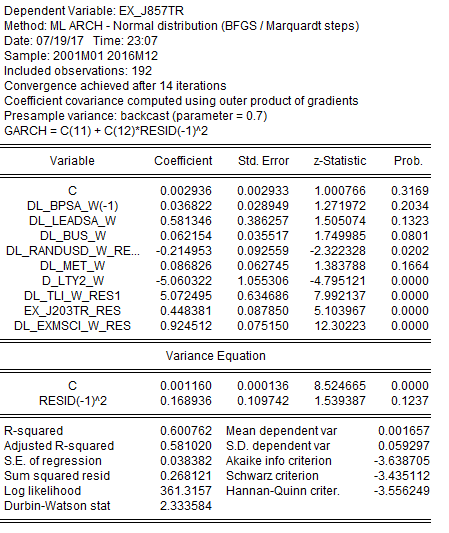

My second unrestricted version is:

In the unrestricted model, ex_j203tr_res and dl_exmsci_w_res are orthogonal to the other factors. However, when I include these factors, the estimated coefficients change. Under OLS, this does not happen - the addition of the orthogonal factors does not impact any of the coefficient estimates.

Why is this happening under ARCH/GARCH estimation?

I am under the impression that when factors that are orthogonal are, there is be no impact on existing estimated coefficients? This seams to hold under OLS but not maximum likelihood?